Investment Report 2023")

Key finding

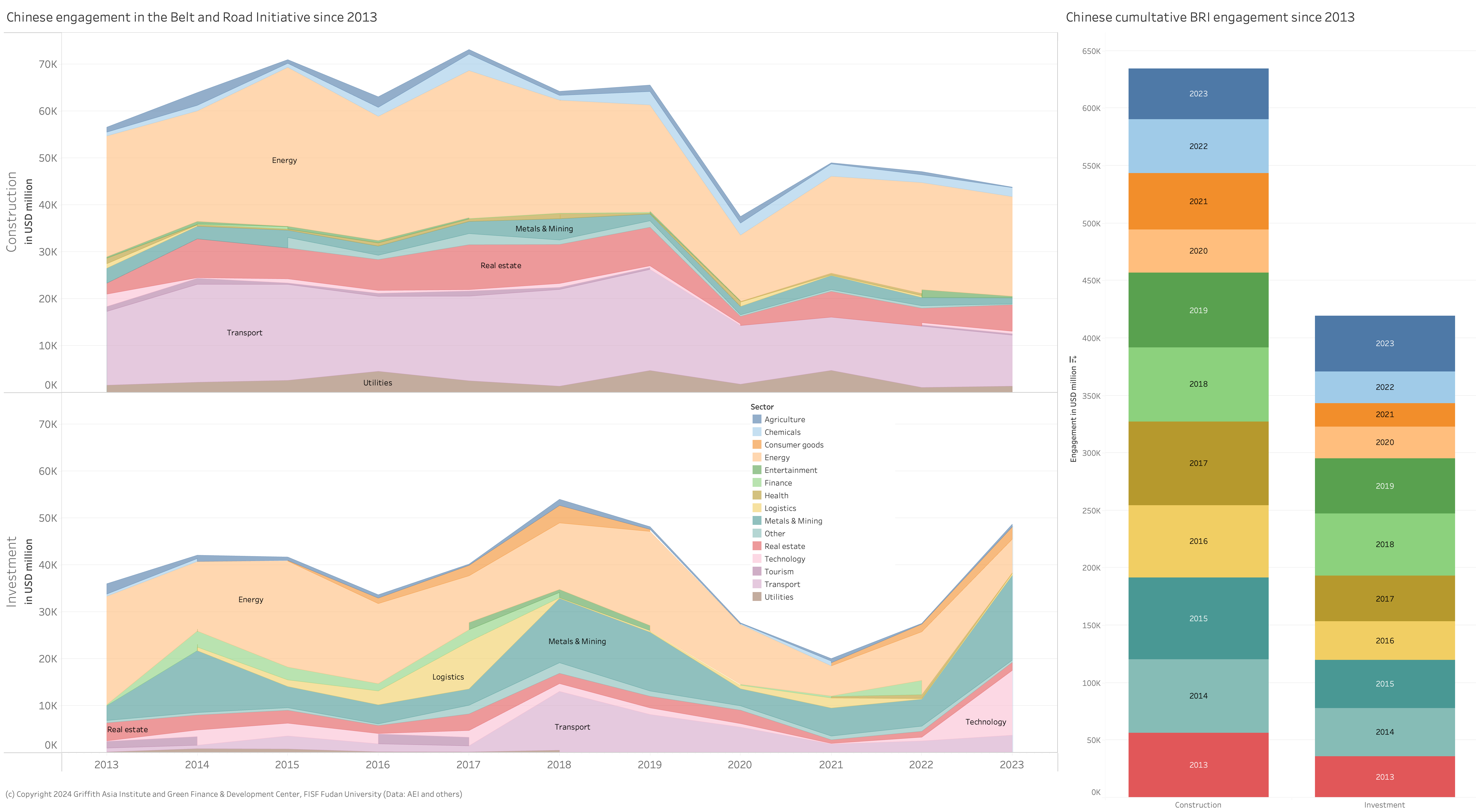

- 10 years after the announcement of the Belt and Road Initiative (BRI), cumulative BRI engagement breached the USD 1 trillion mark (USD1.053 trillion), with about USD634 billion in construction contracts, and USD419 billion in non-financial investments

- China’s energy related engagement in 2023 were the greenest in absolute and relative terms in any period since the BRI’s inception reaching USD7.9 billion;

- China is increasingly investing in electricity transmission (over USD7 billion);

- BRI finance and investments has picked up in 2023 with about 212 deals worth USD92.4 billion compared to about USD74.5 billion in 2022;

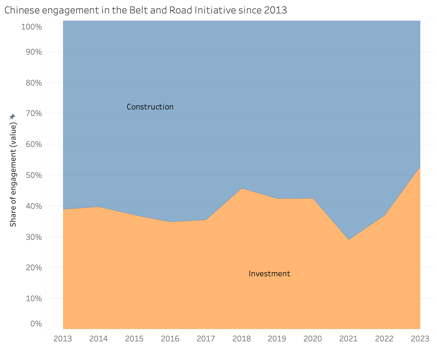

- Investments as a share of BRI engagement reached record levels at over 52%, indicating higher ownership and risk taking of Chinese enterprises;

- In 2023, particularly the technology (+1046%) and metals and mining (+158%) grew.

- Chinese companies strongly invest in metals and mining, which are particularly relevant to the green transition (e.g., lithium) and batteries for electric vehicles.

- Engagement related to batteries reached about USD8 billion;

- Africa became the largest recipient of Chinese engagement, overtaking Middle Eastern countries;

- 19 countries saw a 100% drop in BRI engagement, including Turkey, and Kenya; Russia saw one deal in 2023, after no engagements in 2022;

- BRI investments in 2023 continue to be dominated by private sector enterprises, including Huayao Cobalt and CATL, while construction contracts were dominated by state-owned enterprises (SOEs);

- In global comparison, Chinese overseas engagement grew, while global FDI into emerging economies in 2023 dropped significantly;

- For 2024, we see further growth of Chinese BRI engagement with a strong focus on BRI country partnerships in renewable energy, mining and related technologies;

- Potential future engagements can be expected in six project types: manufacturing in new technologies (e.g., batteries), renewable energy, trade-enabling infrastructure (including pipelines, roads), ICT (e.g., data centers), resource-backed deals (e.g., mining, oil, gas), high visibility or strategic projects (e.g., railway).

The study is developed in partnership with Griffith Asia Institute at Griffith University, Brisbane, Australia.

China’s finance and investments in the Belt and Road initiative (BRI)

Cumulative BRI engagement in the full 10 years since the announcement of the BRI in 2013 breached the USD1 trillion mark to reach USD1.053 trillion, about USD634 in construction contracts, and USD419 in non-financial investments.

Preliminary data on Chinese engagement through financial investments and contractual cooperation for 2023 in the 149 countries of the Belt and Road Initiative[1] show about 212 deals worth USD92.4 billion. This compares to USD 74.5 billion BRI engagement in all of 2022 – an increase of 18%).

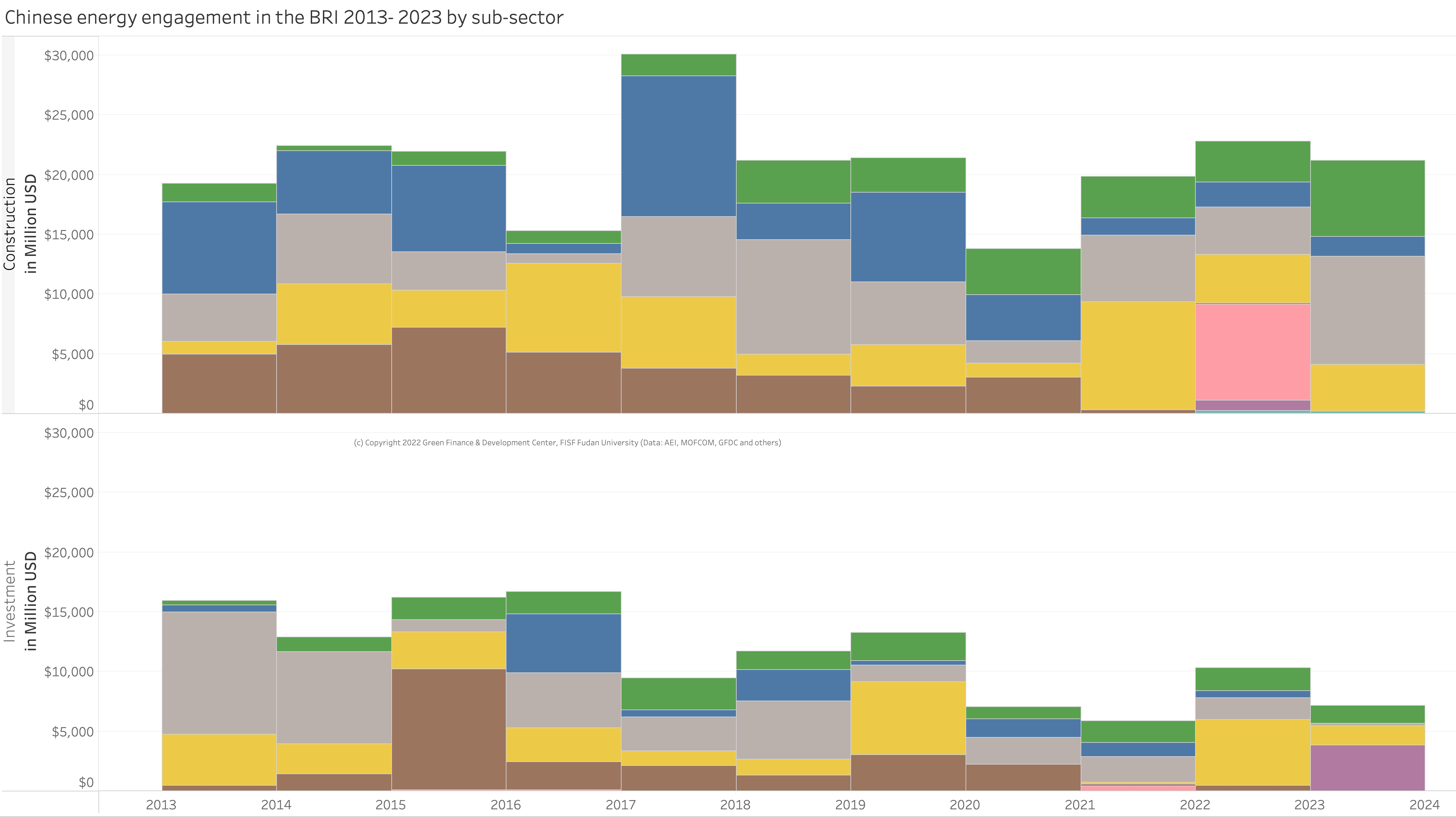

Of the 2023 engagement, about USD44.6 billion was through investment and USD43.7 billion through construction contracts (partly financed by Chinese loans). China’s overall engagement shows a steady development since 2020 from the onset of COVID-19.

| About the data: In November 2023, the Ministry of Commerce (MOFCOM) released new BRI engagement statistics covering the period of January to October 2023. According to these data, Chinese enterprises invested about USD25.85 billion in non-financial direct investments in countries “along the Belt and Road” (a year-on-year increase of 20.1%). At the same time, the value of newly-signed project contracts by Chinese enterprises in the “Belt and Road” countries was USD128.42 billion, a year-on-year decrease of 5%. For this report, the definition of BRI countries includes 150 countries that had signed a cooperation agreement with China to work under the framework of the Belt and Road Initiative by December 2023. This analysis is derived from and presents numbers very similar to the China Global Investment Tracker (CGIT), published by the American Enterprise Institute. We expand those data with our own data based on research at Griffith Asia Institute and at the Green Finance & Development Center affiliated with FISF Fudan University, Shanghai. Specifically, the CGIT includes deals with a size of over USD100 million. We expand the data with more research and granularity for sub-sectors and sub-sectors and adjust, include or exclude projects based on our own information. We define BRI engagements as those Chinese construction and investment deals in countries that had we identify as having an MoU with China to cooperate under the BRI at the time of the report (thus, if the Syrian Republic signed a BRI MoU in 2022, we also count prior investments into Syria as BRI investments). As with most data, they tend to be imperfect and need regular updating. |

Share of investments in China’s BRI highest on record

Cumulative BRI engagement in the full 10 years since the announcement of the BRI in 2013 breached the USD1 trillion mark to reach USD1.053 trillion, about USD634 in construction contracts, and USD419 in non-financial investments.

Preliminary data on Chinese engagement through financial investments and contractual cooperation for 2023 in the 149 countries of the Belt and Road Initiative[1] show about 212 deals worth USD92.4 billion. This compares to USD 74.5 billion BRI engagement in all of 2022 – an increase of 18%).

This compares to construction contracts that are typically financed through loans provided by Chinese financial institutions and/or contractors with the project often receiving guarantees through the host country’s government institutions.

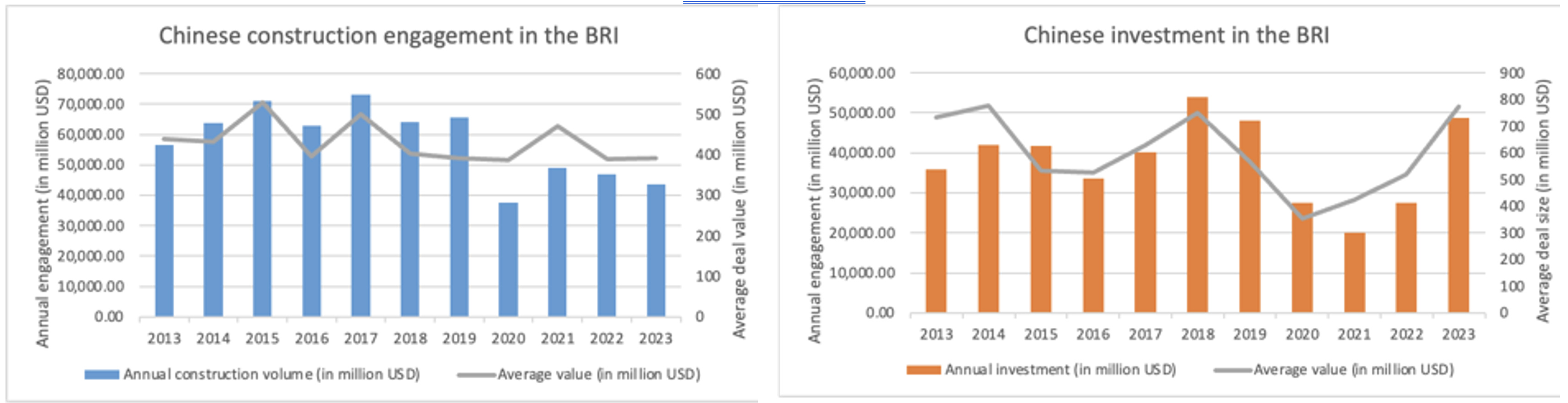

Deal sizes are getting bigger again, particularly for investments

The average deal size for investments has more than doubled from a low or USD354 million in 2020 to USD772 million in 2023. This is the second highest deal size since the BRI’s inception in 2013 (2018 had investment deal sizes of USD749 million).

For construction projects, the deal size in 2023 was the second lowest since the BRI was announced in 2013, with about USD394 million (see Figure 3). Compared to the peak in 2017, this is a 22% decrease.

Particularly for construction projects, this trend is likely in line with the ambition to have “small or beautiful projects” in the BRI propagated through official channels. Another reason is that China adjusted its risk management strategies to adjust for BRI country risks that are more pronounced, e.g., due to sovereign debt issues.

Regional and country analysis of Chinese BRI engagement

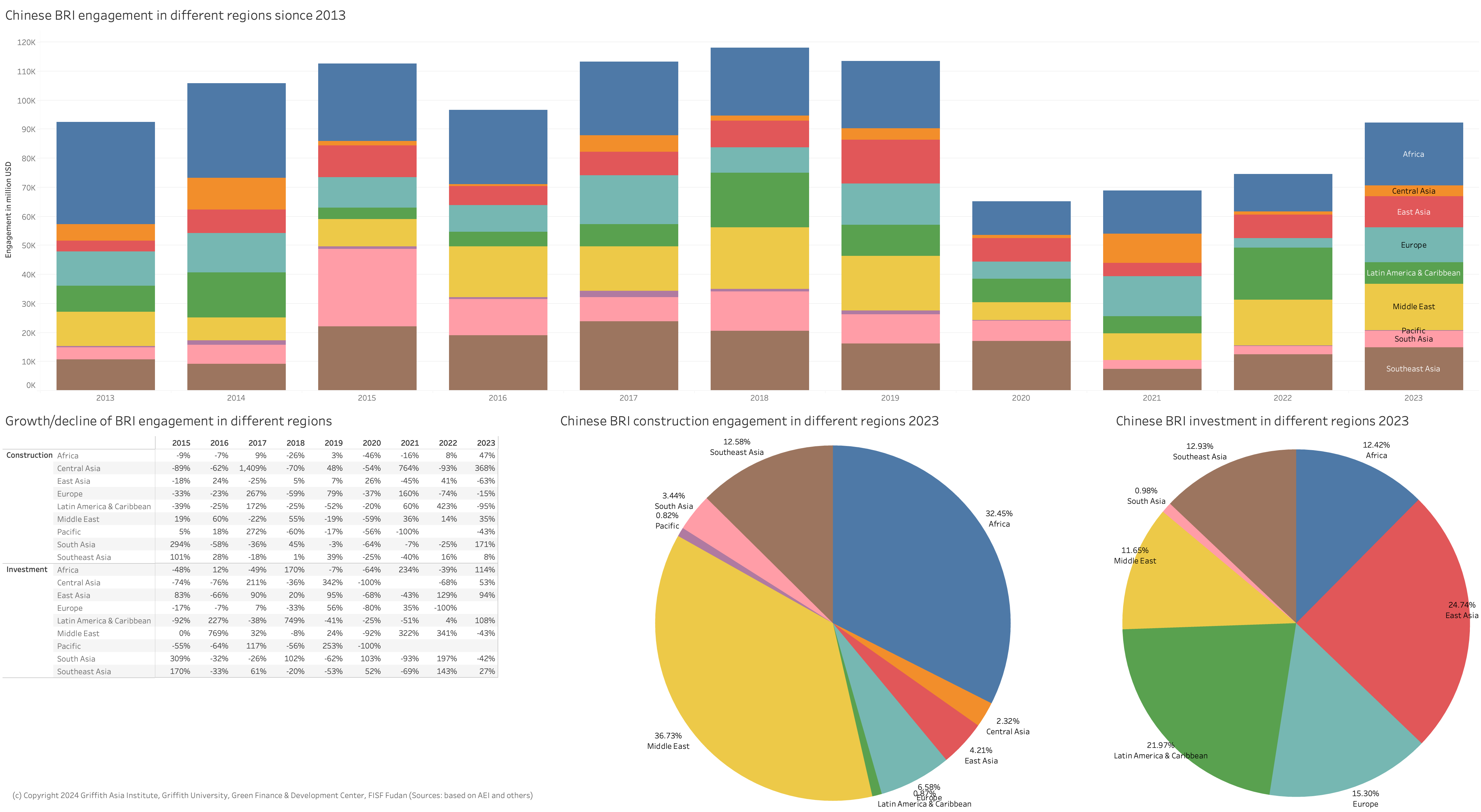

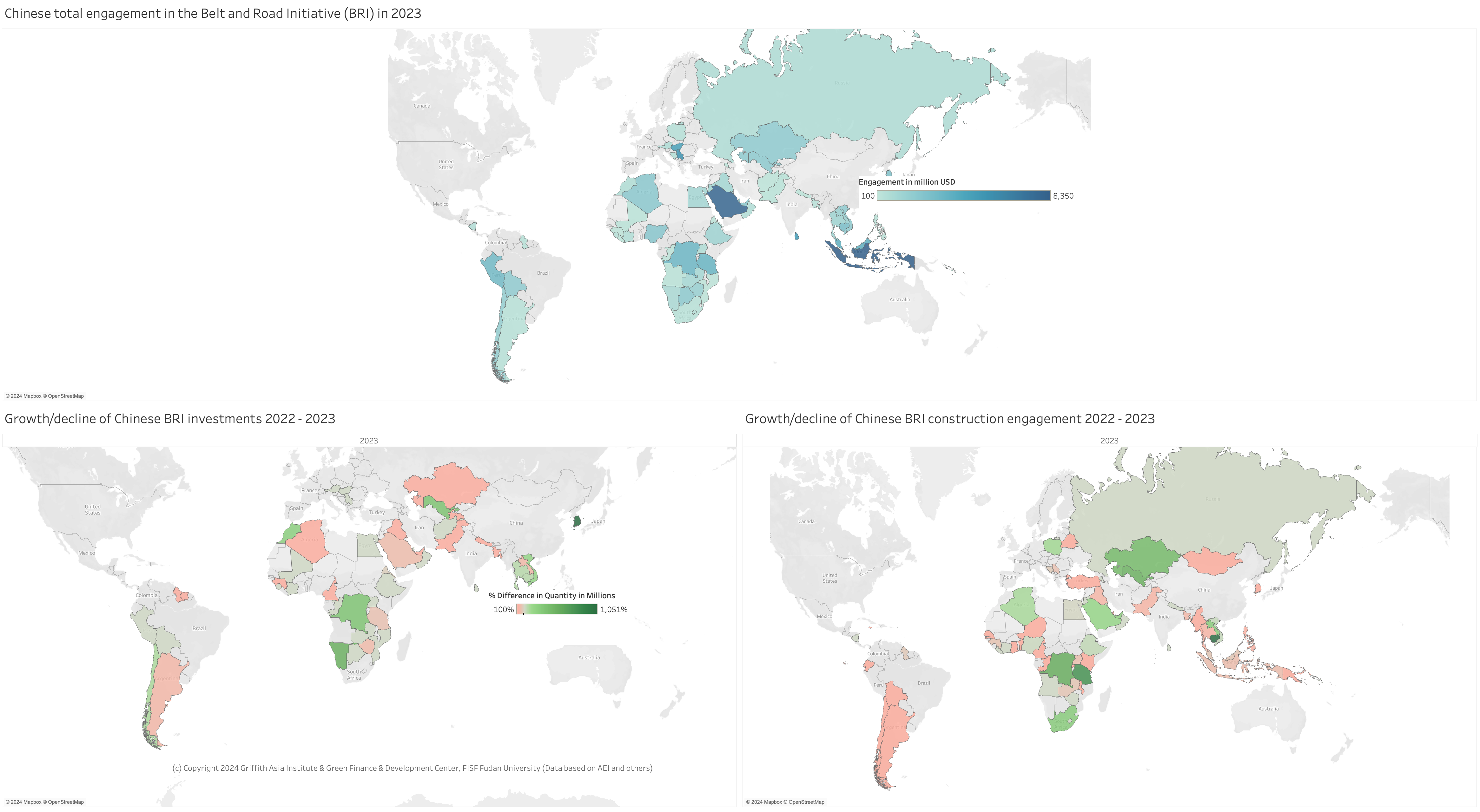

Africa as the largest recipient of BRI engagement with strong growth also in Central Asia

Chinese BRI engagement was not evenly distributed among all regions. BRI countries in Africa saw a 47% increase in Chinese construction contracts and 114% increase in investments. In consequence Africa as a continent became the largest recipient of Chinese engagement worth USD21.7 billion, overtaking Middle Eastern countries that saw USD15.8 billion engagement.

Nevertheless, Middle Eastern countries continued to be a major recipient of Chinese construction engagement, receiving 36.7% of total BRI construction engagement in 2023, a growth of 31% from 2022.

East Asian BRI countries, meanwhile, expanded its intake of Chinese investments by 94% to USD6.8 billion in 2023.

Interestingly, Latin American BRI countries saw very little construction engagement in 2023, just USD180 million (just ahead of Pacific BRI countries receiving USD170 construction engagement). Yet, Latin American BRI countries saw an increase of 92% for its investments to receive about 5.5 billion in investments, taking 20.5% of all Chinese BRI overseas investments.

China’s financing and investment spread across 61 BRI countries in 2023 (up from 60 in 2022), with 37 countries receiving investments and 45 with construction engagement.

The country with the highest construction volume in 2023 was Saudi Arabia, with about USD5.6 billion (up from 2.6 billion in 2022), followed by Sri Lanka (USD4.5 billion), Tanzania (about USD3.1 billion) and UAE (USD2 billion).

Regarding BRI investments, Indonesia was the single largest recipient with about USD7.3 billion in investments, followed by Hungary (USD4.5 billion) and Peru (USD2.9 billion).

19 countries saw a 100% drop of BRI engagement compared to 2022, including Kenya, Myanmar, Turkey. China’s engagement in Pakistan for the China Pakistan Economic Corridor (CPEC) dropped by about 74% (see Figure 5).

The countries with the largest growth of BRI engagement were South Korea (+577 %), Bolivia (+493%), Namibia (+457%), Tanzania (+415%), and Uzbekistan (+375%).

After Russia did not receive any Chinese engagement in 2022, China National Chemical Engineering Corporation (CNCEC) joined AEON Corporation to build a methanol plant in Volgograd.

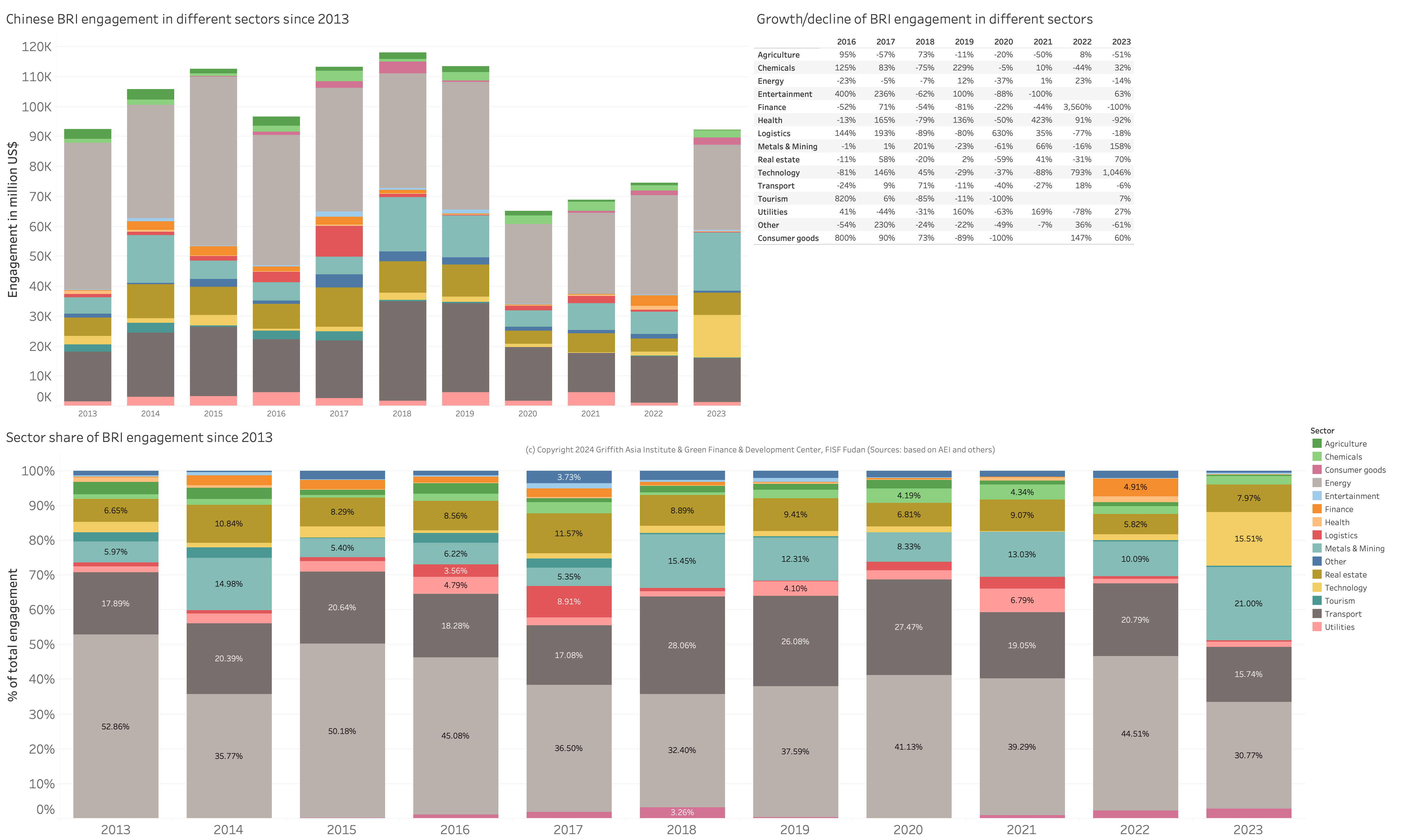

Sector trends of BRI engagement

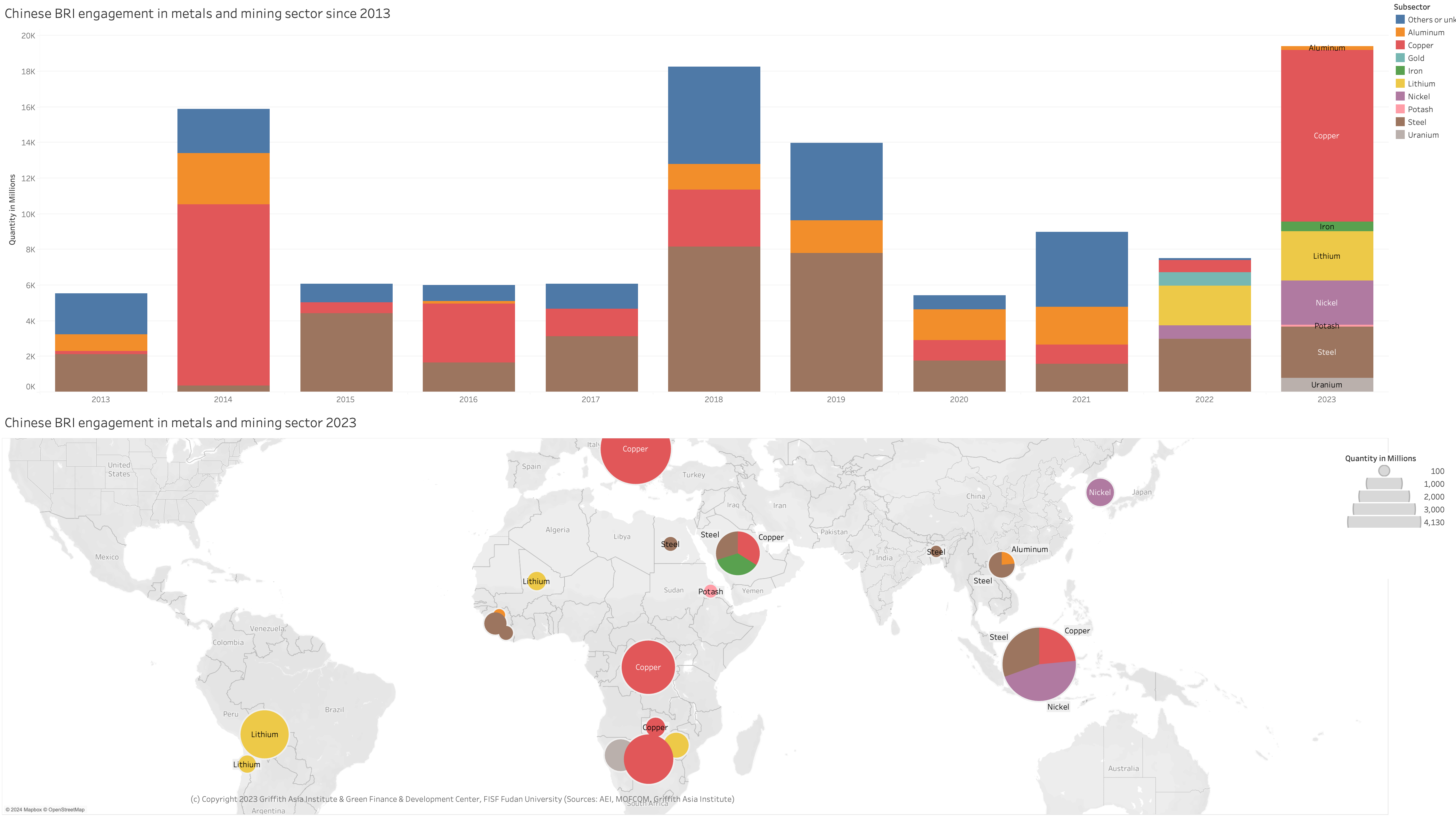

In 2023, particularly the technology (+1046%) and metals and mining (+158%) grew compared to 2022.

The focus of China’s overseas BRI engagement continued to be in infrastructure, particularly in energy (31%) and transport (16%), which is a significant reduction particularly in the energy sector (down from 45% in 2022). The mining sector overtook the transport sector, constituting 21% of Chinese overseas engagement.

| About technology: in 2023, we summarized all electric vehicle and car-related investments into technology, which were previously partly located in the transport sector. |

Finance, utilities and health sectors saw significant drops.

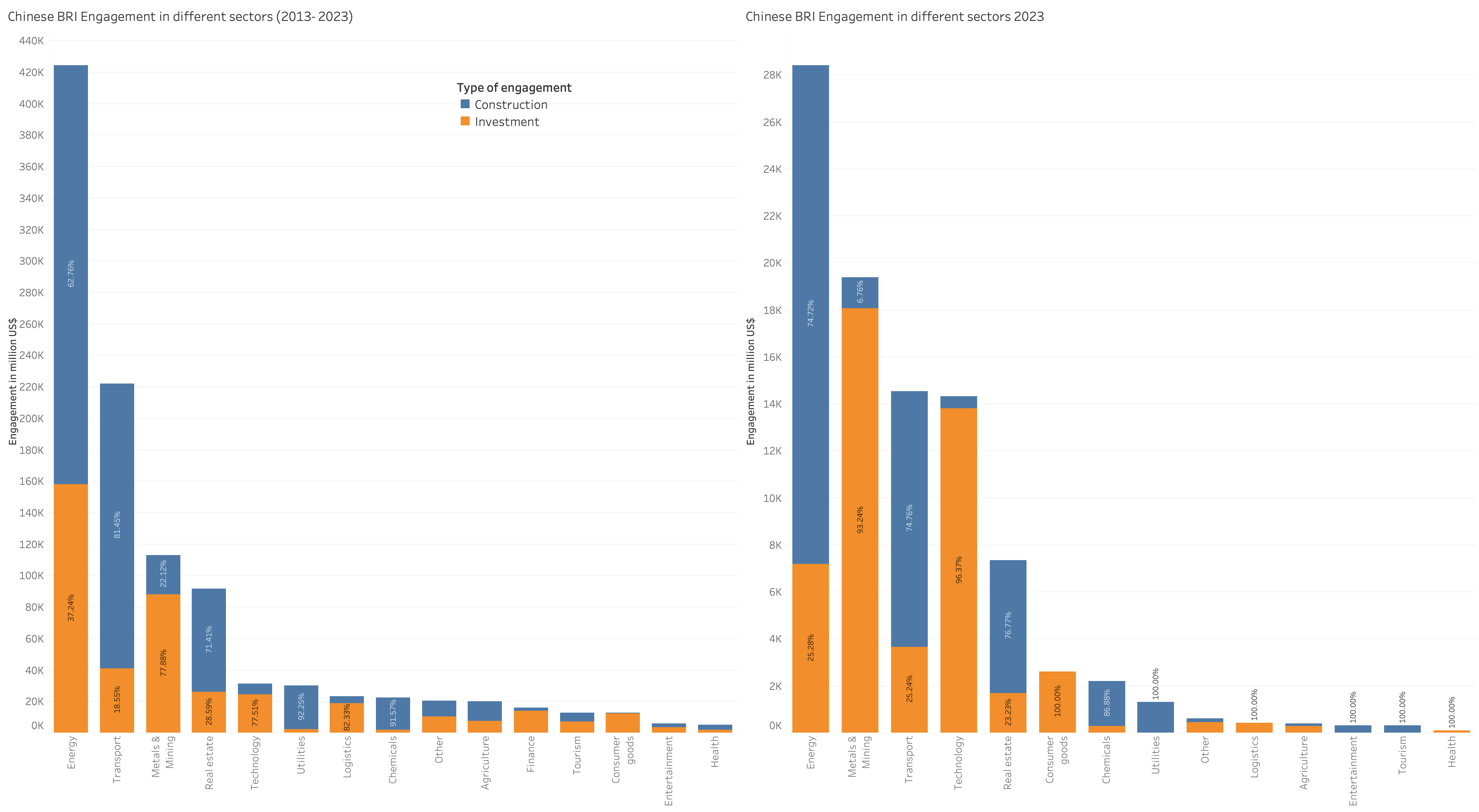

When looking at China’s engagement strategy in these sectors distinguished by construction and investment, it becomes clear that investment with equity shares and thus higher risk within the Chinese organizations becomes an increasingly important strategy particularly in mining, technology, and transport.

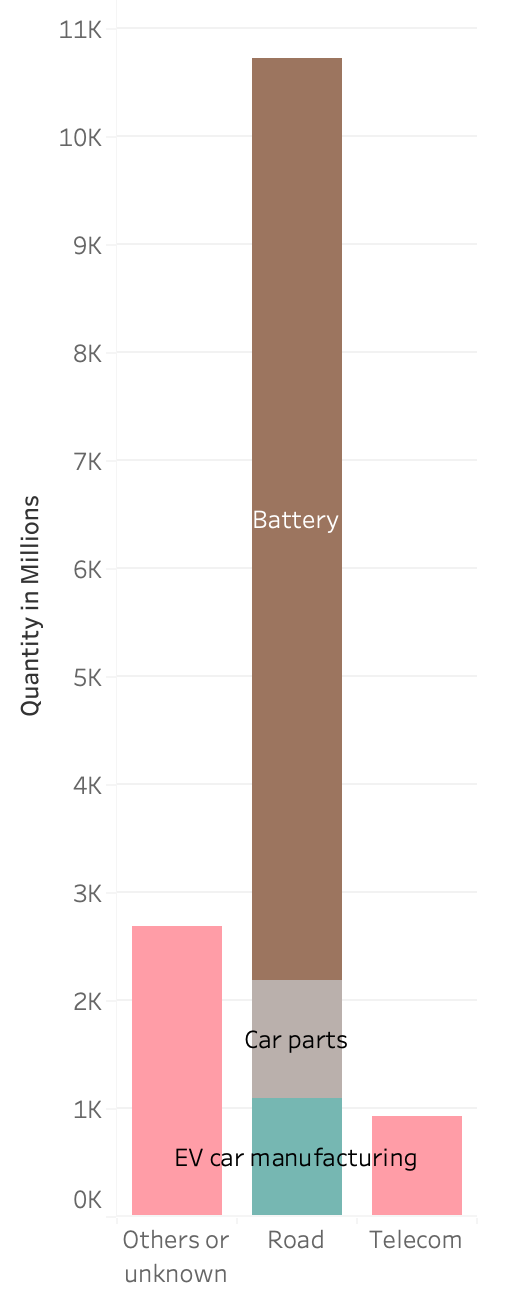

One important growth sector is technology which reached over USD14.3 billion engagement in BRI countries with a focus on battery, car parts, EV manufacturing, as well as telecoms (see Figure 8). Some noteworthy engagements include investments into electric vehicles, such as battery production with Zhejiang Huayou Cobalt in collaboration with LG in South Korea, or Zhejiang Hezhong’s EV car manufacturing in Thailand. Outside of the BRI, BYD established a car manufacturing in Brazil.

A manufacturing plant related to renewable energy technology was the Goldwind agreement for the implementation of a wind turbine industrial unit worth around USD36 million, which will generate about 1,100 direct and indirect jobs.

In Indonesia, Tria Solar, Sinar Mas, Agra Surya Energi and Indonesia’s government-owned power company PLN agreed to construct Indonesia’s largest solar cell and solar panel factory in Central Java.

Another important growth area of strategic importance is China’s engagement in metals and mining reaching USD19.4 billion. Engagement in the sector has grown by 158% compared to 2022 and reached the highest level since 2013. The minerals and metals are particularly relevant to the green transition (e.g., lithium) and batteries for electric vehicles. Engagement has been strong in various African countries, Bolivia and Chile in Latin America, and Indonesia. China already holds significant shares of global mining sources (e.g., over 80% of global graphite resources), and even more control in material processing (where across lithium, nickel, cobalt and graphite, China owns more than 50% of global capacity).

Examples include vertical integration investments by the world’s largest battery manufacturer CATL, which bought the share’s for a nickel mining concession in Indonesia from PT Aneka Tambang Tbk (Antam).[8] Others are a lithium mining operation in Mali by Jiangxi Ganfeng or through Hainan Mining’s acquisition of Kodal Minerals part of a lithium mine in Mali, a copper processing plant agreement in Saudi Arabia, and a commissioning of a lithium processing plant in Zimbabwe.

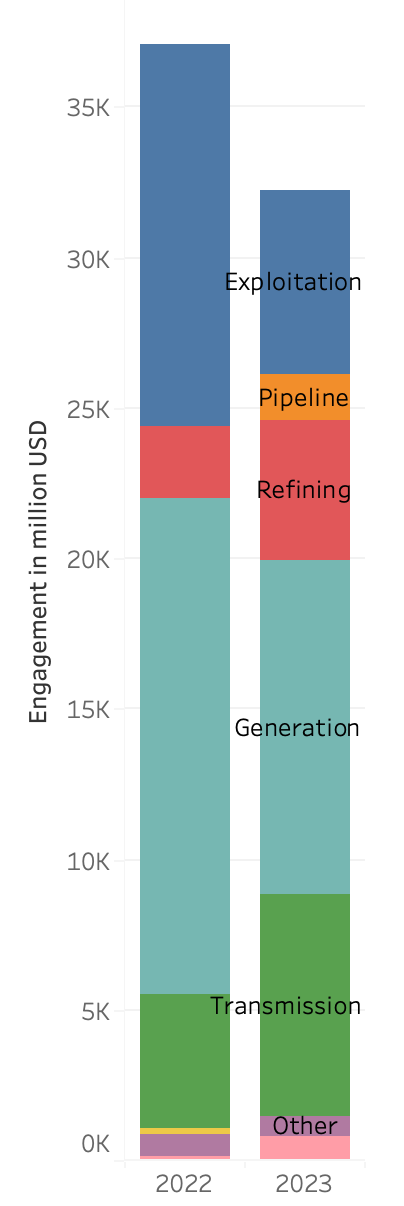

Energy-related engagement in the BRI at low levels but with green growth including transmission

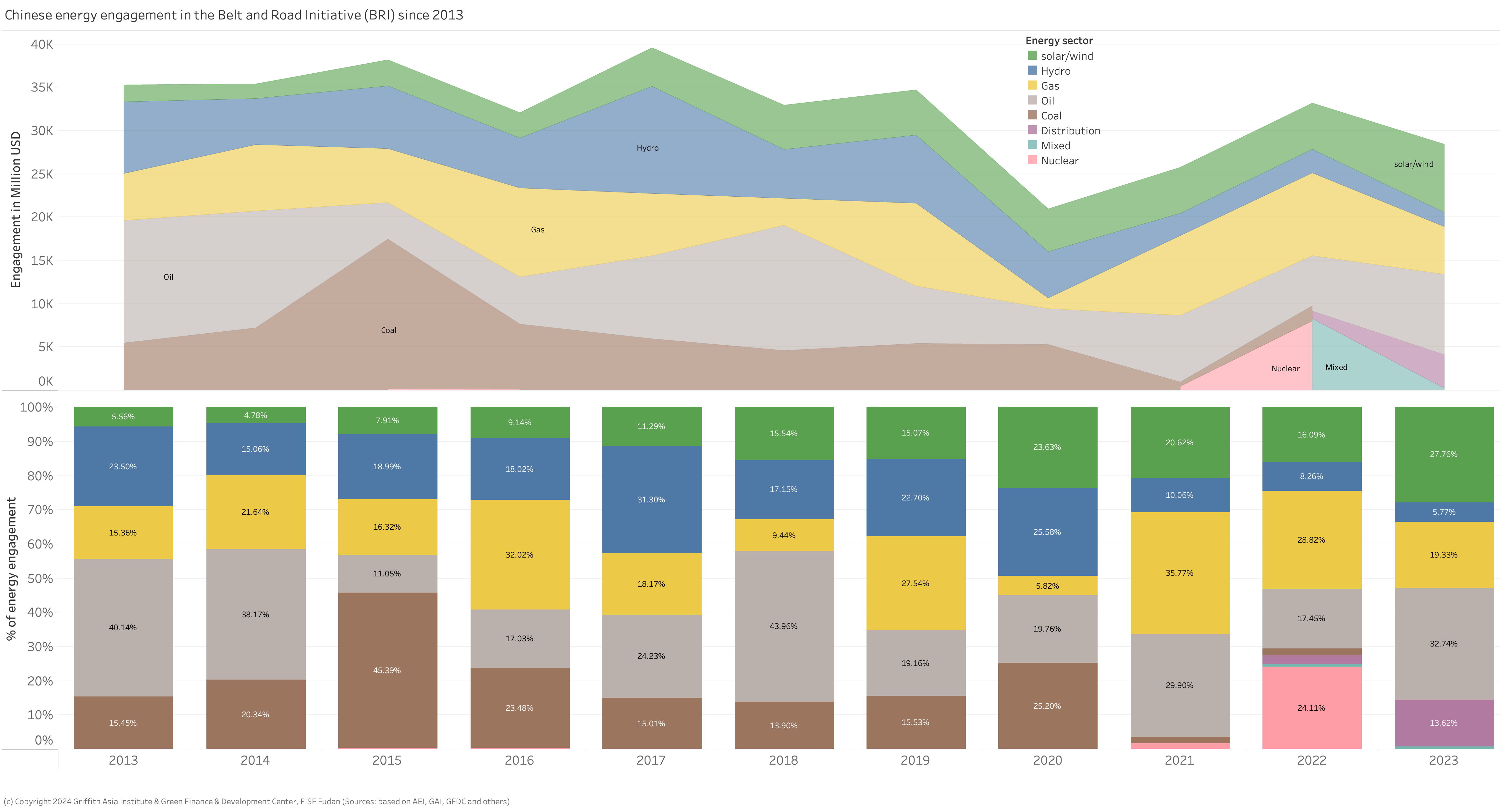

China’s energy related engagement in 2023 was the greenest since the BRI’s inception in 2013: in 2023, China’s green (solar, wind) energy engagement was about USD7.9 billion, about 28% of energy engagement, plus an additional 6% (USD1.6 billion) into hydropower.

| Starting with this report, we include energy-related transmission engagement. |

Chinese engagement related to the energy sector constitutes the largest share of China’s BRI engagement. In 2023, total engagement in the energy sector reached short of USD30 billion – which is the lowest BRI energy engagement except for 2020.

A particular development is increased green energy (solar, wind and biomass) engagement, which reached records of USD 7.9 billion (this number does not include Chinese export of solar equipment).

Also, engagement in distribution systems (e.g., substations, power lines) constituted more than 11% of Chinese BRI energy engagement.

Coal

Following China’s announcement in September 2021 to not to build new coal fired power plants, select new coal-fired power projects seem to progress.

In January 2024, a new 380 MW coal-fired power plant unit, Labota No. 7 built by Chinese companies, started operation, the Pakistan government approved a 300 MW of coal fired power in Gwadar, Pakistan in January 2023 to be constructed by China. While Pakistan had announced in December 2020 to not build new coal-fired power plants, various sources report that China was interested in providing financial and technical support for the project – including the design that requires import of coal (rather than using possibly more affordable domestic coal in Pakistan). However, no financial closing has been announced, which is why this project is not included in the 2023 dataset.

Oil and gas

Oil and gas engagement fell slightly to USD15.7 billion (52% of Chinese overseas energy engagement), USD6.4 billion in gas and 9.3 USD billion in oil.

A major deal was the USD4.5 billion engagement by Sinopec in Sri Lanka to build an oil refinery, which was approved in November 2023.

Rumors of an 8 GW gas power plant in Yakutia, Russian Far East, with China’s Power China from June 2023 have not yet been confirmed.

Oil-related investments dropped to zero in 2023 after years with several higher profile projects inside and outside the BRI (e.g., China’s CNOOC engaged in a USD1.9 billion production sharing deal with Petrobras to explore Brazil’s Buzlos field).

At the same time, BRI partners invested in China to support oil development, such as Aramco’s investment in a petrochemical complex in Panjin City, Liaoling Province.

Green energy/hydropower

China’s total engagement in green energy (solar and wind) and hydropower amounted to about USD9.5 billion in 2023. This compares to USD8.1 billion in 2022 (see Figure 10).

Looking at investment only, Chinese green energy and hydropower investment decreased to USD1.5 billion in 2023 from USD2.1 billion in 2022.

Meanwhile, construction projects related to green energy (including hydropower) increased from USD5.6 billion in 2022 to USD8.1 billion in 2023.

Energy engagement across the supply chain

China’s engagement across the energy supply chain has evolved in the dataframe from 2022 to 2023. While in both years, energy generation was most important for China’s BRI engagement, exploitation (particularly in oil and gas) has decreased significantly from USD12.7 billion to USD6.1 billion. Meanwhile transmission engagement, crucial for the green transition, has increased from USD4.5 billion to over USD7 billion.

Energy engagement in different countries

Analyzing Chinese energy engagement in different BRI countries, we find that, Sri Lanka took the top spot due to Sinopec’s engagement in building an oil revinery. Similar to 2022, also Saudi Arabia held a top spot as the country that received the most energy engagement in 2023 (USD3.7 billion), followed by Peru (USD2.9 billion). Contrary to previous year, Saudi Arabia also received a significant share (19%) of green energy engagement. Peru, meanwhile, received all of its engagement in transmission projects, where China Southern Power Grid International bought the distribution, supply, and energy services assets from Italian energy company Enel.

Overall, the most important partners for China’s BRI energy engagement since the BRI’s initiation in 2013 remains Pakistan, which has received USD28 billion through investment and construction contracts (most of which in hydropower and coal). Pakistan is followed by Russia and Saudi Arabia.

An interesting case for China’s energy investment is Zimbabwe: after a cancelled coal-fired power plant in 2021, Zimbabwe saw strong engagement in green energy through an agreement on a 1GW floating solar station in 2023.

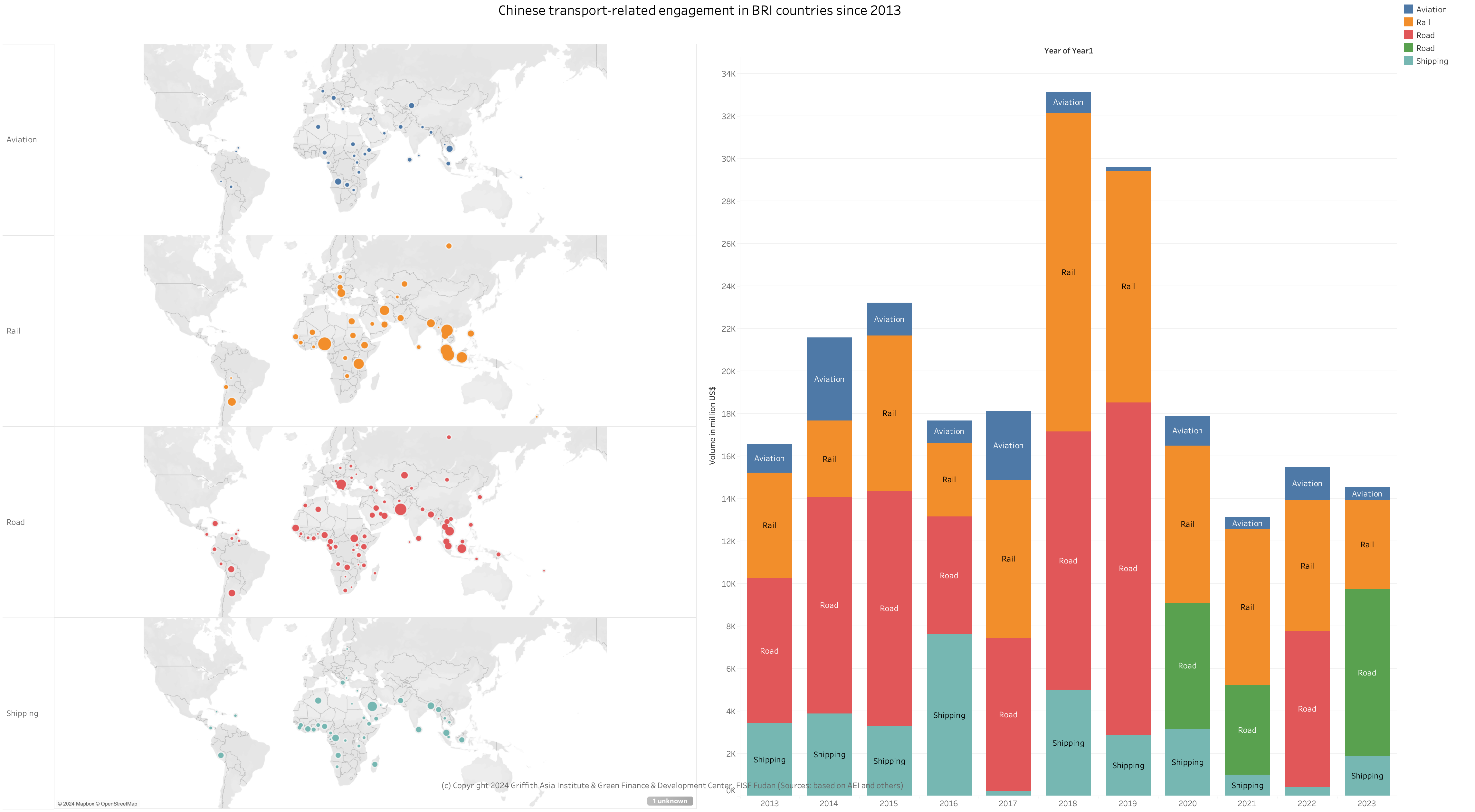

Transport engagement in the Belt and Road Initiative

Transport-related engagement is key to providing the means to trade between China and the BRI countries – where trade is a core component of the BRI. Accordingly, China has invested in and constructed projects in road, rail, aviation, shipping, and logistics across the world.

Aviation: Two projects were announced, including the upgrade of the runway of Honiara Airport in Solomon Island by China Railway Construction.

Rail: Total rail engagement was worth USD4.2 billion (all but one through construction contracts) with engagements in Africa, Latin America and East Asia, such as the Kinshasa urban railway in the Democratic Republic of Congo.

Also, China engaged through its CRRC to manufacture rail wagons and wheels in Saudi Arabia.

Other noteworthy projects include an agreement on the tram project in Colombia.

Road-transport: China continues to engage in road construction projects across many countries worth USD7.5 billion. Examples include a toll road in Cambodia worth about USD1.6 billion.

Ports: Some shipping and port-related projects investments were announced in 2023, such as an agreement with Saudi Arabia to support Aramco’s corporations shipping projects.

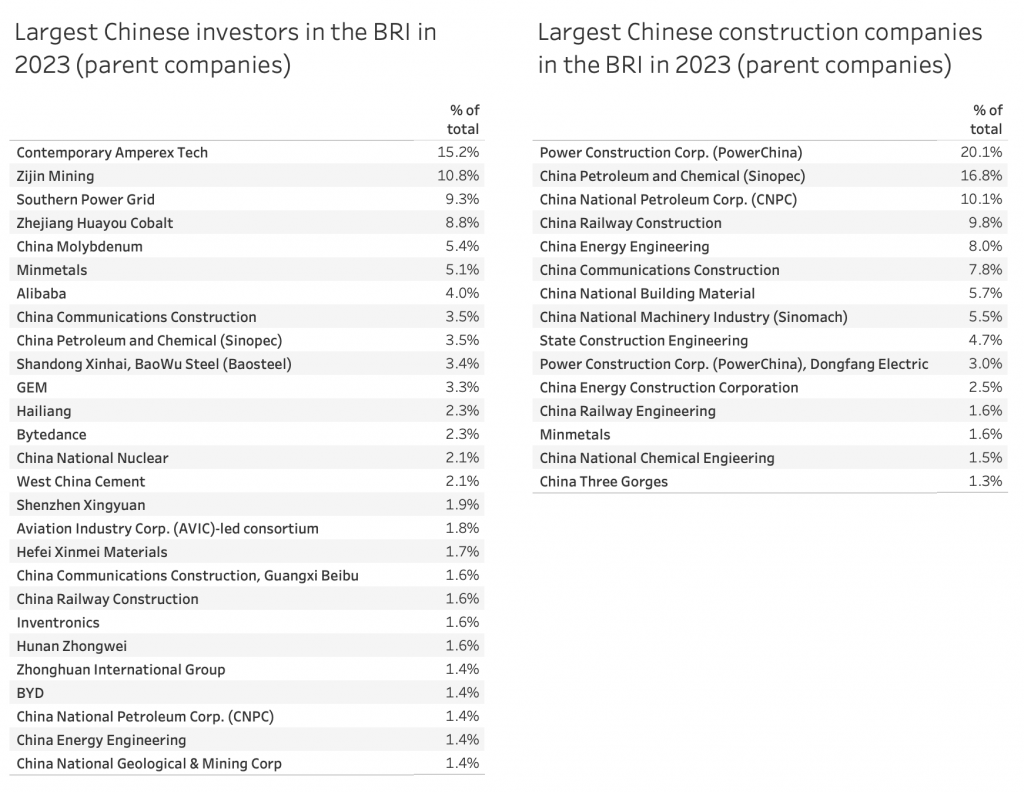

Major players in BRI investments

Among the major players for BRI investments in 2023 were – contrary to most years before – not exclusively Chinese SOEs, but private enterprises.

For investment projects, Contemporary Amperex Tech (CATL), the world’s largest battery producer, led ahead of Zhejiang Huayou Cobalt (both private companies)

The Chinese companies most prominently featured in construction projects in the BRI in 2022 was Power China, followed by China Petroleum and Chemical (Sinpoec) and China National Petroleum Corp (CNPC). This development for construction projects is in line with last years’ trends.

China’s BRI investments in a global comparison

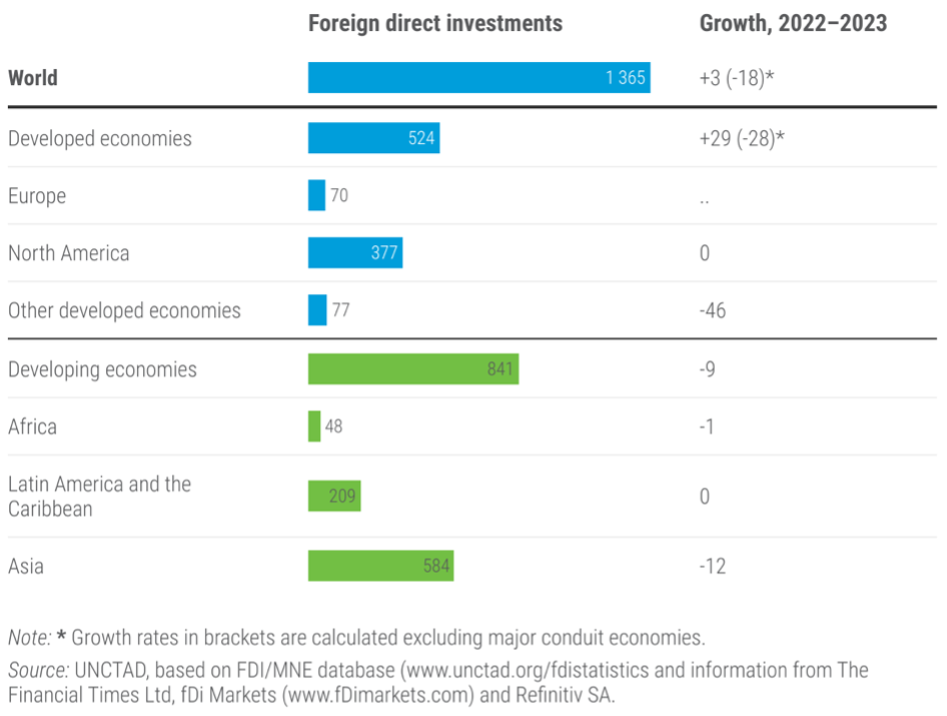

Foreign direct investments (FDI) to developing countries fell to USD841 billion in 2023, a drop of 9%, according to UNCTAD’s Global Investment Trends Monitor, published in January 2024.

Particularly developing countries in Asia saw a steep decline of FDI, registering a 12% drop. FDI into Africa and Latin America, meanwhile, remained more stable.

In Asia, developing economies remained nevertheless attractive destinations for greenfield projects, despite drops of FDI of 6% in China and 47% in India. Similarly, ASEAN economies saw a decline of 16% – despite a 37% increase in greenfield investments.

Middle Eastern countries saw a rise in greenfield announcements, led by a 28% increase of FDI in the UAE.

African FDI flows, meanwhile stayed stable at an estimated USD48 billion with strong engagement in Morocco, Kenya, and Nigeria. An issue seemed to have been infrastructure engagements, which dropped by more than 30% in Africa.

Also Latin American economies saw a decrease in FDI, such as a drop of FDI by 22% in Brazil (particularly project finance).

Worrisome is the first decline (17%) in international project finance deals for renewable energy since the Paris Agreement.

Looking ahead, UNCTAD expects a modest increase in FDI flows in 2024 with moderate inflation and tempered borrowing cost. However, geopolitical risks, and high debt levels remain a concern for global FDI flows.

Outlook for Belt and Road Initiative (BRI) Finance and Investments

Chinese finance and investments into the Belt and Road Initiative countries in 2023 have accelerated.

For 2024, a further recovery of BRI investments and construction contracts seems possible. On the one hand, there is clear need for investments to green boost growth to support the green transition both in China and in BRI countries. This provides great opportunities for mining and minerals processing deals, technology deals (e.g., EV manufacturing, battery manufacturing) and green energy (e.g., energy production and transmission). China refers to these industries (electric vehicles, batteries and renewable energy) as the “New Three“.

Furthermore, continuing post-COVID19 investments by global financial institutions, including developing finance institutions (such as the World Bank, Asian Development Bank, AIIB) provide infrastructure development opportunities for Chinese contractors.

We do expect Chinese BRI engagement to reach levels at least as high in 2024 as in 2023. Part of this expectation is driven by challenges in China’s domestic economic development, where Chinese companies seek opportunities in other countries.

In line with our previous predictions, we continue to see deal numbers increasing. With strong engagement in sectors requiring significant investment (e.g., mining, manufacturing), compared to sectors with variable engagement (e.g., renewable energy), we can expect deal size to also remain larger than in 2021 and 2022.

At the same time, we see two types of large strategic project types to continue that might not have direct financial benefits: transport infrastructure engagements (such as in strategic rail and road to connect mines), and resource-backed deals (such as in oil, gas pipelines).

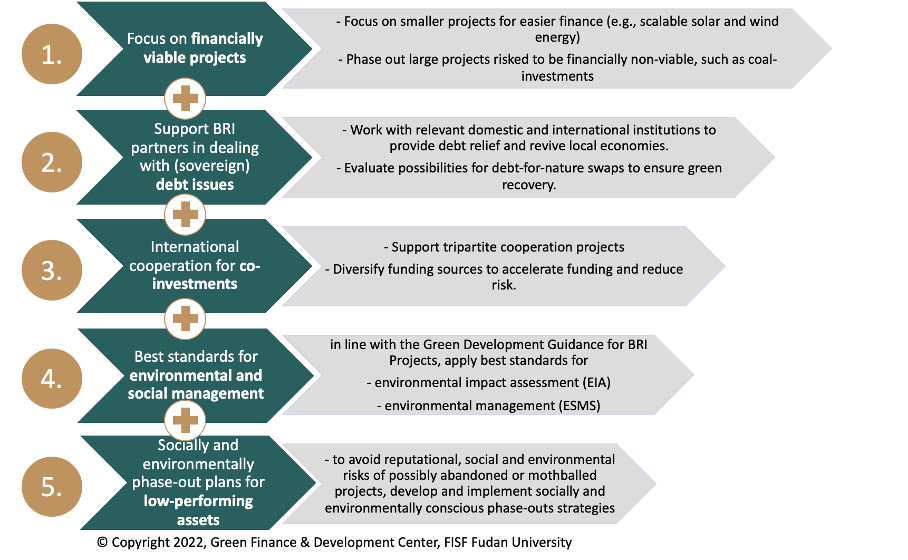

To move the BRI investments forward, we expand our recommendations from the previous reports:

Figure 16: 5-step framework for accelerating green BRI investments

1. Focus on projects that are financially sustainable and cut losses in non-profitable projects

Investors in BRI projects within China and outside China should focus on smaller projects that are easier to finance and faster to implement. Particularly in infrastructure and energy investments, scalable solar and wind investments seem viable, as long as local conditions provide the relevant grids to handle renewable energy supply.

With decreasing energy cost for renewable energy, we also see an opportunity to invest in early phase-out of existing older coal projects, which would be both economically and environmentally relevant.

2. Support partner-countries and partner businesses in dealing with (sovereign) debt-repayment of already invested BRI projects, e.g., through debt-for-nature swaps and nature performance bonds.

Debt is a major concern for future growth in many BRI countries. As we found in our in-depth analysis of debt in BRI countries, China has a unique opportunity to support BRI countries in dealing with their debt both bilaterally and multilaterally. Dealing with the debt issue is crucial for providing BRI countries with the necessary fiscal space for future investments.

While debt-for-resource or debt-for-equity swaps might seem beneficial for China in the short-term to reduce the debt burden in the BRI countries, these swaps tend to undermine future domestic growth opportunities for BRI countries. Rather, Chinese relevant stakeholders together with international partners through multilateral frameworks should support green recovery by swapping part of the debt for nature and providing necessary frameworks to increase transparency and accountability of the use of funds.

Furthermore, sustainable debt instruments could be applied to raise more funds, e.g., through nature performance bonds.[26]

3. Increase international cooperation for BRI projects to allow existing and useful projects to go ahead also in difficult times.

Tripartite cooperation with international financial and implementation partners can support BRI projects through better access to financial resources, risk sharing and knowledge sharing. Particularly non-SOEs that often have a higher burden of accessing investments from Chinese large financial institutions could benefit through broader access to finance, as witnessed for example in the Zhanatas wind farm in Kazakhstan, co-financed by EBRD, AIIB, GCF and ICBC, while it was build and is operated by China International power Holding[27]. Also, Chinese financial institutions could benefit to de-risk project finance by broaden their international cooperation. A report “China Third-Party Market Cooperation for Infrastructure Finance Financing Mechanism Handbook” had been released in September 2021 to accelerate tri-partite project finance.[28]

In addition, with European Union (EU) launching its “Global Gateway” and the US pushing its “Partnership for Global Infrastructure” (PGI), competition for the BRI is increasing. However, if cooperation for project finance and development in emerging markets is the goal, Chinese investors and developers can accelerate their cooperation with both public and private financial institutions from various economies, particularly if they manage to share standards.

4. Increase use of common environmental and social standards in project evaluation (e.g., environmental impact assessment EIA) and for environmental and social risk management (ESMS)

In July 2021, the Ministry of Commerce (MOFCOM), together with the Ministry of Ecology and Environment, issued the Guidelines for Greening Overseas Investment and Cooperation”[29] and in January 2022, the Guidelines for Ecological Environmental Protection of Foreign Investment Cooperation and Construction Projects”[30]. Within these Guideline, Chinese developers are encouraged to adhere to international or Chinese environmental standards, particularly in countries whose domestic environmental standards and governance does not meet international standards.

This is a formalization of a number of previous Guidances, including the “Green Development Guidance for BRI Projects Baseline Study” and the “Application Guide for Enterprises and Financial Institutions” backed by various relevant Chinese ministries published by the BRI Green Development Coalition (BRIGC) in December 2020 and October 2021 respectively. These guidances calls for Chinese overseas investors to apply independent environmental impact assessments (EIA) and strict environmental and social risk management (ESMS) to ensure projects and investments are minimizing environmental harm and maximizing environmental benefits. Also, the Green Investment Principles (GIP) integrate sustainability into corporate governance, requiring boards to understand environmental, social and governance risks, as well as disclosing environmental information.

By applying international standards, Chinese financial institutions can more easily raise capital on the global capital markets, accelerate co-financing with international partners and take responsibility to fulfill the goal of building a “Green Belt and Road”.

5. Develop socially and environmentally conscious phase-out strategies for non-performing investments

Several investments in the Belt and Road Initiative have had to be stopped, mothballed or cancelled due to financial (e.g., difficulties in financing or servicing debt) and operational reasons (e.g. due to travel restrictions or problems in supply chains). According to our study, over 50% of announced coal fired power plants have been mothballed. In order to avoid reputational, social and environmental risks arising from stopped, mothballed or cancelled projects, plans should be developed and implemented by financial institutions including insurance companies, developers, local governments and relevant Chinese authorities that compensate any losses to workers and companies up to a specific extent, and that ensure that nature around mothballed and particularly stopped projects can be remediated. This also helps avoid having skeleton constructions serve as a reminder of unfinished projects.

Dr. Christoph NEDOPIL WANG is the Founding Director of the Green Finance & Development Center and a Visiting Professor at the Fanhai International School of Finance (FISF) at Fudan University in Shanghai, China. He is also a Professor at The University of Queensland and the lead for Asia Pacific Industry Transitions.

Christoph was a member of the Belt and Road Initiative Green Coalition (BRIGC) of the Chinese Ministry of Ecology and Environment. He has contributed to policies and provided research/consulting amongst others for the China Council for International Cooperation on Environment and Development (CCICED), the Ministry of Commerce, various private and multilateral finance institutions (e.g. ADB, IFC, as well as multilateral institutions (e.g. UNDP, UNESCAP) and international governments.

Christoph holds a master of engineering from the Technical University Berlin, a master of public administration from Harvard Kennedy School, as well as a PhD in Economics. He has extensive experience in finance, sustainability, innovation, and infrastructure, having established the Green Belt and Road Initiative Centre at the International Institute of Green Finance (IIGF) in Beijing, having worked for the International Finance Corporation (IFC) for almost 10 years and being a Director for the Sino-German Sustainable Transport Project with the German Cooperation Agency GIZ in Beijing.

He has authored books, articles and reports, including UNDP's SDG Finance Taxonomy, IFC's “Navigating through Crises” and “Corporate Governance - Handbook for Board Directors”, and multiple academic papers on capital flows, sustainability and international development.

2026 H1")

")