Investment Report 2024")

Key findings

- 2024 saw the highest BRI engagement ever, with USD70.7 billion in construction contracts and about USD51 billion in investments;

- China’s energy related engagement in 2024 were the greenest in absolute and relative terms in any period since the BRI’s inceptionreaching USD11.8 billion, an increase of 60% compared to 2023;

- Oil and gas engagement surged to record highs of about USD24.3 billion, particularly through oil/gas processing facilities construction contracts in the Middle East;

- China continued to invest in coal-related activities, both in construction of coal mine transport infrastructure and in coal mine ownership;

- Middle Eastern countries topped the rank of BRI engagement, reaching USD39 billion. Meanwhile Latin American BRI countries saw their lowest Chinese engagement in almost 10 years – with significant drops in Chinese investments;

- Metals and mining sector reached new records of almost USD 22 billion – mostly through investments;

- The technology and manufacturing also broke records and reached almost USD30 billion with high-tech engagements in batteries, solar PV and – outside of the BRI in Spain – in hydrogen;

- BRI investments in 2024 were back to state-owned domination led by Sinopec yet followed by private companies. Construction contracts continue to be dominated by state-owned enterprises (SOEs);

- In global comparison, Chinese overseas engagement grew, while global FDI into emerging economies in 2024 continued to drop (driven by a drop of FDI into China);

- Since its establishment in 2013, cumulative BRI engagement reached USD 1.175 trillion, with about USD704 billion in construction contracts, and USD 470 billion in non-financial investments;

- For 2025, we see further stabilization of Chinese BRI engagement with a strong focus on BRI country partnerships in renewable energy, mining and related technologies;

- Global trade and investment volatility will potentially spur further investment for supply chain resilience and alternative export markets for Chinese companies

- Potential future engagements are unchanged in six project types: manufacturing in new technologies (e.g., batteries), renewable energy, trade-enabling infrastructure (including pipelines, roads), ICT (e.g., data centers), resource-backed deals (e.g., mining, oil, gas), high visibility or strategic projects (e.g., railway).

China’s engagement in the Belt and Road Initiative

2024 saw a record year of Chinese BRI engagement with USD70.7 billion in construction contracts and about USD51 billion in investments. Cumulatively, Chinese BRI engagement has reached USD 1.175 trillion since 2013. Preliminary data on Chinese engagement through financial investments and contractual cooperation for 2024 in the 149 countries of the Belt and Road Initiative show about 340 deals worth USD121.8 billion. This compares to USD 92.3 billion BRI engagement in all of 2023 – an increase of 31%.

| About the data: In January 2025, the Ministry of Commerce (MOFCOM) released new BRI engagement statistics covering the period of January to November 2024 . According to these data, Chinese enterprises invested about USD29.5 billion in non-financial direct investments in countries “along the Belt and Road”. At the same time, the value of newly-signed project contracts by Chinese enterprises in the “Belt and Road” countries was USD113 billion, as well as 700 aid projects. For this report, we define BRI engagements as those Chinese construction and investment deals in countries that had we identify as having an MoU with China to cooperate under the BRI at the time of the report (thus, if the Syrian Republic signed a BRI MoU in 2022, we also count prior investments into Syria as BRI investments). The definition of BRI countries thus includes 149 countries that had signed a cooperation agreement with China to work under the framework of the Belt and Road Initiative (BRI) by December 2024. Data until 2023 were reliant on and significantly expanded from the China Global Investment Tracker (CGIT), published by the American Enterprise Institute . Starting with data for 2024, we follow a rigorous independent collection process where we include projects with validated credible sources or two independent sources. We include projects with a signed contract for implementation or clear announcements of investments (e.g., stock market announcements). We more consistently include projects from about USD20 million, rather than projects with at least USD100 million in volume in the CGIT. Where we see that this inclusion might lead to different data interpretation, we included a separate calculation. As with most data, they tend to be imperfect and need regular updating. |

Share of investments in China’s BRI drops amid high construction contracts

The share of Chinese engagement in the BRI through investments compared to construction dropped in 2024 and reached about 42% of BRI engagement compared to 53% in 2023 and about 29% in 2021. This compares to construction contracts that are typically financed through loans provided by Chinese financial institutions and/or contractors with the project often receiving guarantees through the host country’s government institutions potentially backed up by resources (e.g., oil, gas).

Deal sizes are getting smaller for investments and larger for construction

The average deal size for investments with a value larger than USD100 million shrank from USD772 million in 2023 to USD672 million in 2024[1]. This is above average for the past 10 years.

For construction projects, the average deal size in 2024 increased due to some very large deals (e.g., USD8 billion oil refinery deal in Iraq) stable and increased slightly to USD498 million, up from USD394 in 2023.

Particularly for construction projects, this trend is bucking the ambition to have “small yet beautiful projects” in the BRI propagated through official channels. However, it is important to note (as seen later in the report) that most large infrastructure projects are resource-backed deals (e.g., oil, gas) rather than fiscal spending deals (e.g., road construction).

|  |

Regional and country analysis of Chinese BRI engagement

Middle East as the largest recipient of BRI engagement with strong growth also in the Pacific

Chinese BRI engagement was not evenly distributed among all regions. While China expanded construction engagement across all regions except South Asia (minus 64%), particularly the Pacific saw a 228% increase in Chinese construction contracts – albeit from a low starting point. The region saw no significant investment from China.

Meanwhile an increase of 102% of construction engagement in the Middle East catapulted the region to become China’s most important partner in 2024 with a total engagement of about USD39 billion. In consequence Africa as a continent dropped to second place with USD29.2 billion engagement, a growth of 34% of Chinese total engagement.

Despite relatively slow growth for China’s engagement in South-East Asia by only 7%, total engagement reached USD25.1 billion.

East Asian BRI countries, meanwhile, significantly expanded their intake of Chinese construction engagement and now constitutes 3.67% of Chinese total construction engagements. Latin American BRI countries saw their lowest Chinese engagement in almost 10 years – with significant drops in Chinese investments (and small growth in construction engagement in 2024).

China’s financing and investment spread across 87 BRI countries in 2024 (up from 79 in 2023), with 53 countries receiving investments and 72 with construction engagement.

The country with the highest construction volume in 2024 was Saudi Arabia, with about USD18.9 billion (up from 5.9 billion in 2023), followed by Iraq (USD 9 billion) United Arab Emirates (USD3.1 billion), and Liberia (about USD3 billion).

Regarding BRI investments, Indonesia was again the single largest recipient with about USD9.3 billion in investments, followed Saudi Arabia (USD5.8 billion), and Kazakhstan (USD 4.6 billion).

11 countries saw a 100% drop of BRI engagement compared to 2023, including Cote D’Ivoire, Sierra Leone, Armenia, and Jordan. China’s engagement in Pakistan for the China Pakistan Economic Corridor (CPEC) dropped by 40%, after dropping about 74% in the previous period.

The countries with the largest growth of BRI engagement were Guinea (+1,935 %), Liberia (+1,900%), Republic of Congo (+1,800%), Iraq (+799%), and Morocco (+724%). While in 2022, the year of Russia’s invasion of Ukraine, Russia did not receive any Chinese engagement, China’s engagement in the country remained low with about USD212 million.

Sector trends of BRI engagement

In 2024, particularly the energy sector (+ USD11.5 billion), the technology sector (+USD5 billion) and metals & mining (+2 billion) grew compared to 2023. The focus of China’s overseas BRI engagement continued to be in energy (33%). Compared to early years of the BRI, the transport sector dropped to its lowest level of only 12% share of BRI engagement. Meanwhile, the mining sector remained the second largest sector with about 17.6% (albeit lower than the 21% of Chinese overseas engagement in 2023) and the technology sector continued to expand.

When comparing construction and investment in different sectors, it becomes clear that in mining and technology, Chinese firms are increasingly prioritizing equity investments, despite the higher risks involved; meanwhile, energy investments continue to be dominated by construction deals rather than equity-based investments.

Technology and manufacturing

Technology and manufacturing have emerged as key growth sectors, with Chinese engagement in BRI countries exceeding USD 30 billion. The investment is mainly focused on EV batteries and EV manufacturing, as well as significant expansion of solar PV manufacturing. Notable engagements include investments into electric vehicles, such as battery production with BYD’s 1.3 billion production facility in Indonesia, and Gotion’s USD1.3 billion investment in Slovakia (together with Slovak partner InoBat). Outside of the BRI, Spain received about USD3.2 billion in hydrogen-related investments .

Metals and mining

Another important growth sector of strategic importance to China is metals and mining, where China’s engagement reached a record-high of USD21.4 billion in 2024, an increase of 10% compared to 2023. Various minerals and metals are particularly relevant to the green transition and batteries for electric vehicles (e.g., nickel, lithium). Engagement has been strong in various African countries, Bolivia and Chile in Latin America, and Indonesia. China already holds significant shares of global mining sources (e.g., over 80% of global graphite resources), and even more control in material processing (where across lithium, nickel, cobalt and graphite, China owns more than 50% of global capacity).

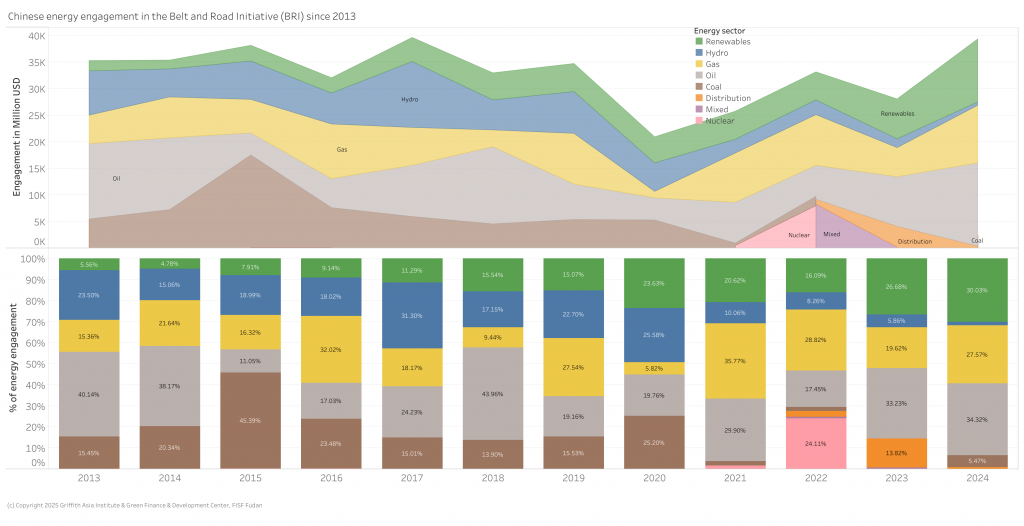

Energy-related engagement in the BRI at highest levels with green growth accelerating

China’s energy–related engagement in 2024 again set a record as the greenest since the BRI’s inception in 2013: in 2024, China’s green (solar, wind, waste-to-energy) energy engagement was about USD11.8 billion, about 30% of China’s total energy engagement, plus an additional USD639 million in hydropower.

China’s engagement in the energy sector represents the largest share of its total BRI engagement. In 2024, total engagement in the energy sector approached USD40 billion, the highest level since 2017.

Two developments stand out: first, China’s engagement in green energy (solar, wind and biomass) reached a record of USD 11.8 billion (excluding solar equipment exports).

Second, China maintained a continued engagement in fossil fuels, particularly gas, but also coal (through coal mining). Also, engagement in distribution systems (e.g., substations, power lines) constituted more than 11% of Chinese BRI energy engagement.

Coal

Following China’s announcement in September 2021 to not to build new coal fired power plants, select new coal-fired power projects seem to progress (e.g., Bangladesh Barisal 2, Gacko II in Bosnia).

While no new coal plants with Chinese participation had been announced since 2021, 2024 saw a resurgence in coal-related engagement through mining operations. PowerChina was engaged in several projects in Mongolia and Bangladesh (through construction contracts) and Zhejiang Energy bought stock in an Indonesian coal mine.

Oil and gas

Oil and gas engagement rose significantly to USD24.3 billion (up from to USD15.7 billion in 2023), constituting 62% of Chinese overseas energy engagement, USD10.8 billion in gas and 13.5 USD billion in oil.

A major deal was the USD8 billion engagement by China National Chemical Engineering in Iraq to build an oil refinery, which was approved in May 2024.

Oil-related investments increased from zero in 2023 to USD1.8 billion through the buy-out of Samsung in the refinery projects Tecnicas Reunidas by Sinopec in cooperation with Tecnicas Reunidas in Algeria.

Green energy/hydropower

China’s total engagement in green energy (solar and wind) and hydropower reached approximately USD11.8 billion in 2024, up from USD9.5 billion in 2023.

Looking at investment only, Chinese green energy and hydropower investment increased to USD1.8 billion in 2024 from USD1.1 billion in 2023. Meanwhile, construction projects related to green energy (excluding hydropower) increased from USD6.4 billion in 2023 to USD10 billion in 2024.

Green energy sources varied

In 2024, a more detailed analysis of green energy sources revealed that China is engaging in a diverse range of renewable energy projects. While solar (46%) and wind (34%) remain most significant, waste-to-energy projects play a notable role (7.34% of all green energy projects), and energy storage is becoming increasingly important.

Energy engagement across the supply chain

Since 2022, China’s engagement across the energy supply chain has evolved significantly. While energy generation remained the primary focus in both 2022 and 2023, 2024 saw a resurgence of fossil fuel processing facilities (USD 17.1 billion) and pipeline projects (USD 4.6 billion). Meanwhile, energy transmission, which is crucial for the green transition, has declined sharply from USD 7.4 billion in 2023 to under USD 500 million.

Energy engagement in different countries

An analysis of China’s energy engagement across BRI countries in 2024 reveals that Saudi Arabia took the lead, driven by nearly USD 6 billion of construction contracts in gas projects involving Sinopec, CNPC and PowerChina, as well as over USD1.6 billion in renewable energy investment. Iraq was the second largest recipient of Chinese BRI energy engagement based on an USD8 billion oil refinery construction deal. Uzbekistan saw a very green energy engagement from China through multiple solar, wind, storage and waste-to-energy plants. Overall, Saudi Arabia has surpassed Pakistan as the most important partner for China’s BRI energy engagement since the BRI’s inception in 2013, receiving about USD 30 billion engagement compared to Pakistan’s USD28 billion, most of which are in hydropower and coal. Iraq now ranks third, followed by Russia and Argentina.

Transport engagement in the Belt and Road Initiative

Transport-related engagement has long been a cornerstone of facilitating trade between China and the BRI countries, and trade is a core component of the BRI. To support this, China has invested in and developed projects in road, rail, aviation, shipping, and logistics across the world. Overall, China’s engagement in transport-related projects remained stable at about USD15 billion (despite a decreasing share due to overall larger volumes) – almost exclusively through construction contracts. This figure represents about half the volume seen during the peak years of 2018 and 2019,

Aviation: Two projects were announced totalling USD175 million, including the expansion of the Konstantin Veliki Airport in Nis, Serbia and an expansion of the concourse at Riyhad Airport in Saudi Arabia.

Rail: Total rail engagement (including lightrail and subway) was worth USD9.6 billion. Most of the volume is one subway construction contract worth USD5.6 billion in Saudi Arabia, as well as some smaller contracts in Singapore and Serbia. Another noteworthy project is an agreement on the tram project in Malaysia.

Road transport: China continues to engage in road construction projects across multiple BRI countries, with a total value of USD 3.1 billion in 2024. However, this marks the lowest volume of road-related engagement in BRI history. Examples include a highway in Cameroon worth about USD540 million.

Ports: In the shipping and port sector, several investments were announced in 2024, such as an agreement with Tanzania to construct petroleum storage and the acquisition of 51% stake in Singapore’s NPH by China Merchant Group.

Major players in BRI investments

In 2024, Chinese state-owned enterprises (SOEs) reclaimed a more dominant role compared to private enterprises, reversing the trend of recent years (see Error! Reference source not found.).

For investment projects, Sinopec, China’s energy SOE, led ahead of PT Shengwei New Energy (a private company). The Chinese companies most prominently featured in construction projects in the BRI in 2024 was PowerChina (again), followed by China National Chemical Engineering and China Petroleum and Chemical (Sinopec). This development for construction projects is in line with last years’ trends.

China’s BRI investments in a global comparison

All foreign direct investments (FDI) to developing countries fell to USD854 billion, a drop of 2% in 2024, marking the second year of decline, according to UNCTAD’s Global Investment Trends Monitor, published in January 2025.

Investments in SDG-related projects (e.g., agrifood, water, sanitation) fell 11% globally in 2024.

Particularly developing countries in Asia (including China) saw a steep decline of FDI, registering a 7% drop to USD588 billion, as well FDI into Latin America and the Caribbean (minus 9%). FDI into Africa, meanwhile, grew by 86% to USD 94 billion.

In Asia, particularly China saw a 29% decline in foreign direct investments, whereas India posted a 13% increase. Similarly, ASEAN economies saw a 2% increase of FDI. Greenfield investments picked up in Brazil, Argentina and Colombia despite overall weak performance.

African economies saw a strong growth mostly due to a large project in Egypt worth over USD 40 billion.

Worrisome is the continued decline (31%) in international project finance deals.

Looking ahead, UNCTAD expects a moderate increase in FDI flows in 2025 with moderate inflation and tempered borrowing cost. However, geopolitical risks, and high debt levels remain a concern for global FDI flows, particularly with high uncertainty about the US trade and investment politics.

Outlook for Belt and Road Initiative (BRI) Finance and Investment

Chinese finance and investments into the Belt and Road Initiative countries in 2024 have accelerated significantly.

For 2025, a further expansion of BRI investments and construction contracts seems possible. On the one hand, there is clear need for investments to green boost growth to support the green transition both in China and in BRI countries. This provides continued opportunities for mining and minerals processing deals, technology deals (e.g., EV manufacturing, battery manufacturing) and green energy (e.g., energy production and transmission). China refers to these industries (electric vehicles, batteries and renewable energy) as the “New Three”.

Furthermore, global trade volatilities and uncertainties can spur investments in supply chain resilience and exploration of new markets by Chinese companies. However, risks emerge due to uncertainty of possible activities by global financial institutions with strong US board presence (e.g., World Bank Group, Asian Development Bank), while China dominated development banks (e.g., AIIB, NDB) should provide infrastructure development opportunities for Chinese contractors.

We do expect Chinese BRI engagement to reach similar levels in 2025 as in 2024. Part of this expectation is driven by growing needs of China’s domestic players to invest abroad to seek opportunities in other countries.

In line with our previous predictions, we continue to see deal numbers increasing. With strong engagement in sectors requiring significant investment (e.g., mining, manufacturing), compared to sectors with variable engagement (e.g., renewable energy), we can expect deal size to also remain larger than in 2022 and 2023 and possibly compared to 2024.

Belt and Road Initiative (BRI) countries by region

The following BRI map shows the list of countries that have signed MoUs or are said to be members of the BRI by region used in this report.

About our partner Griffith Asia Institute

Griffith Asia Institute (GAI) at Griffith University, Brisbane, Australia, is an internationally recognized institute providing knowledge, and solutions for sustainable development in Asia-Pacific. With a history of over 20 years, GAI has forged strong partnerships with key decision-makers in business, policy and with research institutions across the region. With over 80 faculty members and 50 adjunct members, GAI works in multidisciplinary teams and draws on a wide range of technical expertise in energy, finance, policy, economics as well as in regional studies including a strong China component (https://www.griffith.edu.au/asia-institute).

GAI is organized in knowledge and regional hubs:

- The Green Transition and Sustainable Development Hub addresses major challenges and opportunities for Asian and Pacific economies in addressing SDGs related to climate, life on land, life in the sea, partnerships, infrastructure and energy.

- The Governance and Diplomacy Hub addresses major challenges and opportunities in the region for peaceful co-existence, diplomacy, inclusive governance, policymaking and institution building.

- The Inclusive Growth and Rural Development Hub addresses major challenges and opportunities in the region regarding currently underserved communities (eg, women, indigenous, youth, rural, or people with disabilities).

- The four regional hubs address major regional and country-specific challenges and opportunities in (1) Southeast Asia, (2) South Asia, (3) Pacific and (4) China and the Region, each with their own hub lead.

[1] If all deal sizes including those smaller than USD100 million are included, the deal size shrunk to USD621 million. For comparison reasons with slightly different data collection approaches since 2024, we focus on deal size larger than USD100 million in this analysis.

Dr. Christoph NEDOPIL WANG is the Founding Director of the Green Finance & Development Center and a Visiting Professor at the Fanhai International School of Finance (FISF) at Fudan University in Shanghai, China. He is also a Professor at The University of Queensland and the lead for Asia Pacific Industry Transitions.

Christoph was a member of the Belt and Road Initiative Green Coalition (BRIGC) of the Chinese Ministry of Ecology and Environment. He has contributed to policies and provided research/consulting amongst others for the China Council for International Cooperation on Environment and Development (CCICED), the Ministry of Commerce, various private and multilateral finance institutions (e.g. ADB, IFC, as well as multilateral institutions (e.g. UNDP, UNESCAP) and international governments.

Christoph holds a master of engineering from the Technical University Berlin, a master of public administration from Harvard Kennedy School, as well as a PhD in Economics. He has extensive experience in finance, sustainability, innovation, and infrastructure, having established the Green Belt and Road Initiative Centre at the International Institute of Green Finance (IIGF) in Beijing, having worked for the International Finance Corporation (IFC) for almost 10 years and being a Director for the Sino-German Sustainable Transport Project with the German Cooperation Agency GIZ in Beijing.

He has authored books, articles and reports, including UNDP's SDG Finance Taxonomy, IFC's “Navigating through Crises” and “Corporate Governance - Handbook for Board Directors”, and multiple academic papers on capital flows, sustainability and international development.

2026 H1")

")