The original article was published on Panda Paw Dragon Claw on 11th January, 2021 and has been updated on Jan 18, 2021.

“When the tide goes out, you see who is swimming naked”! This is a quote coined by Warren Buffet about those who take on too much debt, believing that never-ending economic growth would allow them to service their every higher debt burdens. Alas, with COVID-19, the tide went out fast and companies and countries around the world are now struggling to service their debt.

Yet, while corporate defaults are relatively well regulated, public debt issues are much more complex with no “sovereign bankruptcy” law. As China has become the world’s largest bilateral creditor, this development is extremely relevant for China: many of the emerging markets that China has provided loans for are struggling to service their debt in the aftermath of COVID-19 for two reasons: first, economies contracted, reducing tax-based government revenues; second, governments are required to spend massively on fiscal and monetary stimulus to prop up the flailing economies. To add fuel to the fire, commodity-exporting countries received a triple blow: falling commodity prices have further reduced government and economic incomes.

To work with the highly indebted countries, China has engaged both in the G20 Debt Service Suspension Initiative (DSSI) and has provided debt relief in one form or another on a bilateral basis. However, China currently still lacks a published strategy to deal with the debt issue holistically and together with other creditors. Accordingly, international (and to some extent domestic) pressure to provide a framework for managing its overseas debt and provide fiscal flexibility for the hardest-hit countries has been increasing.

But, as we found in our research: not all countries are equal. In our Briefing on Public Debt in the Belt and Road Initiative (BRI), we analyzed 52 countries that are both DSSI and BRI countries to identify not only highly-indebted countries, but specifically those countries that are exposed to high debt service payments to China in the coming years. We identified ten countries that have become especially vulnerable. In case of acute risk of debt default, they might require negotiations specifically with China.

Debt service outlook to China – a mixed bag

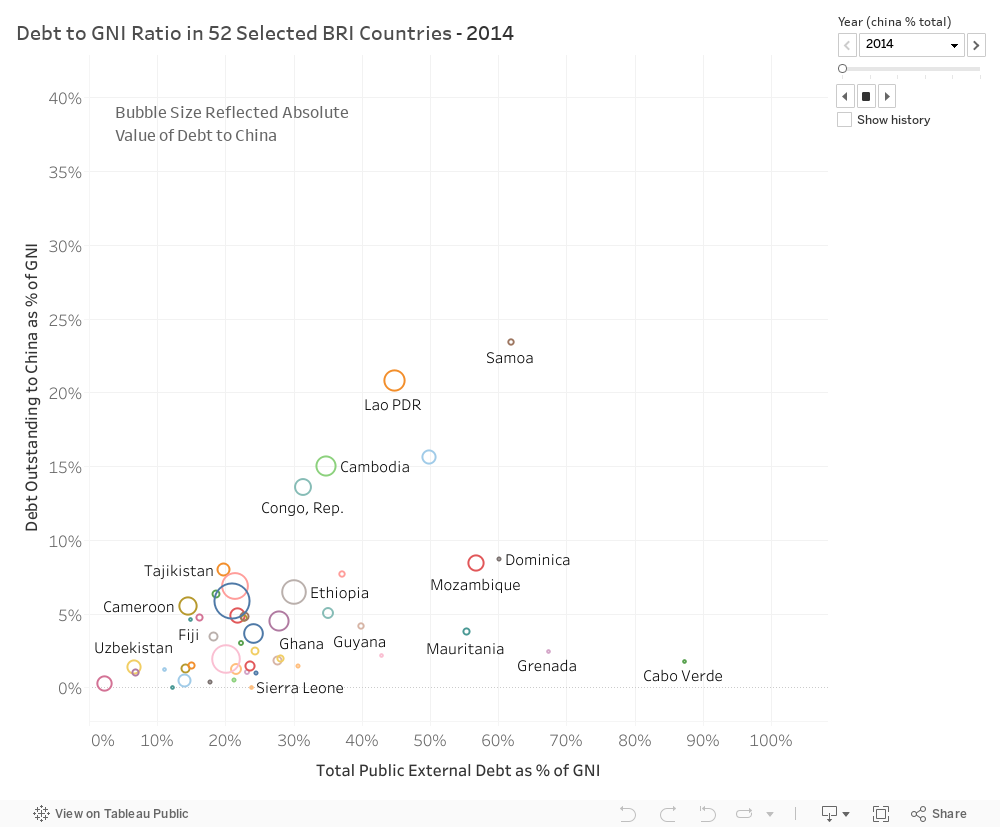

Two notes before we share our findings on the debt service outlook of highly indebted countries to China: first, in our analysis, we found that China’s overseas lending has gone through ups and downs with much growth until 2018 and a steep drop after. Nevertheless, China’s overall share of lending to the 52 countries that we analyzed increased steadily from 16.04% in 2014 to 21.22% in 2019. This makes China by far the largest bilateral creditor in those countries in each year from 2014 to 2019. Second, the debt exposure of these countries to China has not evolved uniformly. While some countries increased their debt exposure to China from 2014 to 2019, such as the Republic of Congo from 13.62% of GNI to 38.92% of GNI, Angola from 5.87% to 18.95% of GNI, other countries leveled off or decrease their debt exposure to China, such as Cambodia, Bangladesh, and others.

Source: World Bank International Debt Statistics; IIGF Green BRI Center (2020)

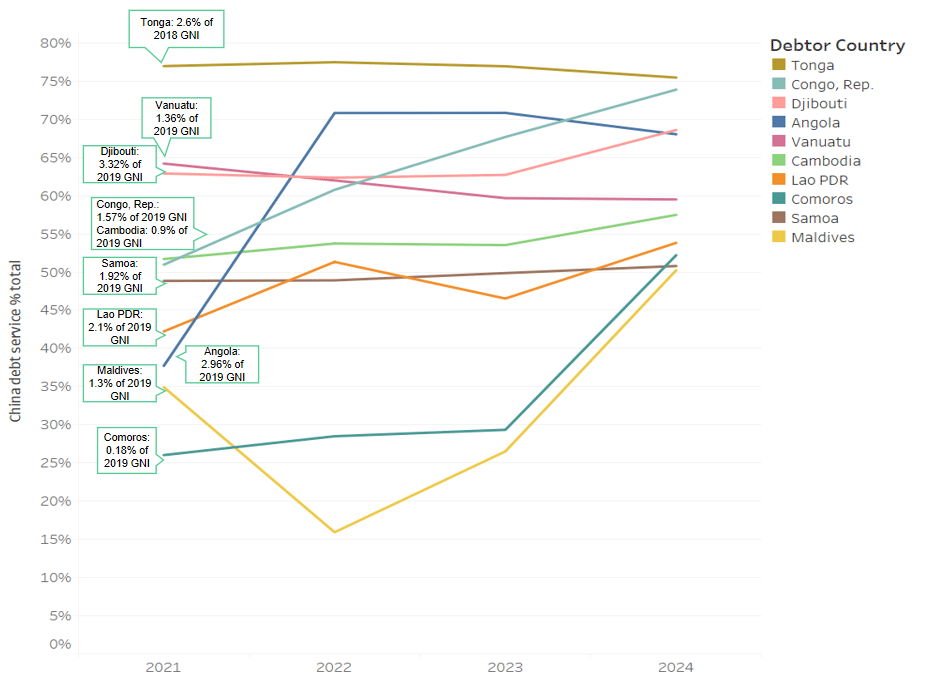

This also impacts debt service to China in the next years. For most countries, projected debt service to China both as a percentage of total debt service, and as a percentage of these countries GNI, remains low or moderate. But there are a few outliers of countries that are particularly exposed to China: Tonga, Vanuatu, Djibouti, Congo Republic, Cambodia, Samoa, Lao PDR, Maldives, Angola, and Comoros will have to pay 25% to 75% of their total debt service to China between 2021 to 2024.

Tonga, Vanuatu, Djibouti, Congo Republic, Cambodia, Samoa, Lao PDR, Maldives, Angola, and Comoros will have to pay 25% to 75% of their total debt service to China between 2021 to 2024.

Tonga, Djibouti, and Cambodia will constantly have to pay more than 50% of their debt-related payments to China. Despite the recent debt restructuring deals with China in Angola and the Republic of the Congo, these two countries will see the shares of debt service to China continue to rise to over 65% of their total public debt service. Comoros and Maldives also need to pay an increasingly large share of annual debt service to China in the next four years.

When looking at the relative amount of those countries’ debt services to China compared to their latest available GNI data from 2019 (which are likely to be up to 30% lower in 2020 and 2021 due to the economic contractions in the COVID-19 aftermath), we find that the size of the expected debt service in the next following years in these countries can be as large 3.3% (in Djibouti). Even using the 2019 GNI numbers, this makes these countries’ debt service to China almost equivalent to their public spending on education!

In other words, for governments of all these ten countries, debt repayment to China will constitute a significant share of their annual fiscal expenditure, while it reduces their fiscal and monetary flexibility to invest in their future.

The need for a comprehensive debt relief framework

To deal with debt, China has to date mostly relied on direct debt cancellation for interest-free loans – and there are signals that China will continue this strategy: The most recent indication was in October when China announced to waive interest-free loans due by the end of 2020 for 15 least-developed African countries, total amount undisclosed.

Responding to the debt challenges in the wake of COVID-19, China signed up to the Debt Service Suspension Initiative (DSSI) under the G20 scheme to suspend bilateral loan repayments for 77 of the world’s poorest countries until the end of June 2021. However, China has to date not announced a comprehensive debt relief program like the members of the Paris Club or multilateral lenders like IMF. Such preference in dealing with debt relief is understandable from China’s view, as it likes to treat each debtor country in its own way. However, this leaves other creditors to those countries in limbo over concerns of hidden risks. Before the debt default of Zambia in November, for instance, bondholders refused a debt freeze because the Zambian government failed to disclose their debt calendar with other creditors, particularly China.

A unique opportunity for China – multilateral, fair, and green

We believe that dealing with the debt in the 10 selected countries can provide a unique opportunity for China, with minimal costs for China paired with high potentials for reputational gains and the possibility to become a global standard setter. Contrary to the high debt burden for these countries, the risk for China is relatively low: according to the World Bank data and our analysis, the total debt outstanding to the 10 countries most vulnerable to payments was US$64.2 billion in 2019, equivalent to only 9.2% of China’s total overseas lending (China’s overseas lending in 2019 was US$696.3 billion according to the State Administration of Foreign Exchange), or 0.2% of its China’s domestic credit market (The size of China’s domestic credit market was US$23.71 trillion in 2019 based on People’s Bank of China statistics).

To use this crisis as an opportunity, we analyzed several recommendations for Chinese policymakers how to deal with the debt. To create necessary liquidity and fiscal space for the respective countries for economic stimulus after COVID-19 and to “build back better”, we found that in the short term, China should

- take the lead in designing emergency plans for debt relief in addition to the G20 Debt Service Suspension for countries with the highest exposure to Chinese debt, such as Djibouti, Republic of the Congo, Lao PDR, Kyrgyzstan, and Angola.

- agree to some level of “haircut”(i.e. sovereign debt write-downs) to its debt to create fiscal space in these countries for the fight against COVID-19 virus with clear stipulations to use the money rather to support a green recovery.

For countries with manageable debt risks and less debt service burden to China, China should engage with multilateral organizations, such as IMF and G20, to provide a common debt restructuring framework.

Debt-for-nature swaps

Contrary to some calls for debt-for-equity and debt-for-resource swaps to reduce debt service burden, we do not agree to either measure under most circumstances: both pathways risk reducing domestic resources for future economic growth. Rather, we suggest for China to engage in debt-for-nature swaps to create triple-win scenarios.

- For China, the largest bilateral creditor in many BRI countries and the host of the 2021 UN Biodiversity Conference, debt-for-nature swaps add value to some of its loans which might otherwise never been repaid and provide an opportunity for China to take the lead in leveraging public and private funding for biodiversity conservation.

- For indebted countries, debt-for-nature swaps could alleviate the burden of repaying loans in foreign exchange, provide funding for the environment and climate projects, as well as contribute to local economy and institutional capacity building.

- For conservation NGOs, debt-for-nature swaps help identify and leverage funding from diverse sources.

Many of the short-term measures should be implemented as soon as possible, with the FOCAC conference planned to take place later this year (most likely online) being an important forum to share the success story.

In the strategic medium- to long term, we recommend for China to support highly indebted countries by providing investments (rather than debt) and capacity building. This means that China’s future engagement should focus less on largesse in infrastructure spending (that often led to an over-indebtedness in those countries), and more on smaller, bankable projects. A possible avenue is green energy investments in solar, wind and in electricity transmission networks: these investments tend to be smaller than those in fossil fuel power plants. Also, green energy investments create about 3-times more jobs than fossil fuel investments, all while generating higher profits for the investor. And of course, they provide the pathway to a zero-emission energy system in line with the climate.

Furthermore, based on successful re-negotiation of debt in the highly vulnerable countries, China should work in multilateral forums such as the G20, FOCAC or the BRI to improve debt governance by setting standards for overseas official lending and designing new debt mechanisms. For this, China needs to clarify the roles of China’s policy banks, particularly China Development Bank (CDB) and China Exim Bank and ideally include them in the DSSI framework. China Development Bank, as one of the most important lenders in the BRI, so far negotiates on the basis of being commercial lender (CDB’s official website defines CDB as a development bank). As such, it has agreed to voluntarily provide debt relief on 748 million USD together with the DSSI. For the future, a clarification of CDB’s role and its continued support for DSSI would be beneficial for internationally coordinated debt-relief.

In any case, for China, to take proactive measures in dealing with its overseas debt is an opportunity that should not be missed.

Dr. Christoph NEDOPIL WANG is the Founding Director of the Green Finance & Development Center and a Visiting Professor at the Fanhai International School of Finance (FISF) at Fudan University in Shanghai, China. He is also a Professor at The University of Queensland and the lead for Asia Pacific Industry Transitions.

Christoph was a member of the Belt and Road Initiative Green Coalition (BRIGC) of the Chinese Ministry of Ecology and Environment. He has contributed to policies and provided research/consulting amongst others for the China Council for International Cooperation on Environment and Development (CCICED), the Ministry of Commerce, various private and multilateral finance institutions (e.g. ADB, IFC, as well as multilateral institutions (e.g. UNDP, UNESCAP) and international governments.

Christoph holds a master of engineering from the Technical University Berlin, a master of public administration from Harvard Kennedy School, as well as a PhD in Economics. He has extensive experience in finance, sustainability, innovation, and infrastructure, having established the Green Belt and Road Initiative Centre at the International Institute of Green Finance (IIGF) in Beijing, having worked for the International Finance Corporation (IFC) for almost 10 years and being a Director for the Sino-German Sustainable Transport Project with the German Cooperation Agency GIZ in Beijing.

He has authored books, articles and reports, including UNDP's SDG Finance Taxonomy, IFC's “Navigating through Crises” and “Corporate Governance - Handbook for Board Directors”, and multiple academic papers on capital flows, sustainability and international development.

Mengdi Yue is a visiting researcher at the Green Finance & Development Center and previously was a researcher at the Green BRI Center at IIGF. She holds a Master in International Relations from School of Advanced International Studies (SAIS) and has worked with the American Enterprise Institute (AEI), European Union Chamber of Commerce in China and the China-ASEAN Environmental Cooperation of the Ministry of Ecology and Environment. She is fascinated by green energy finance in China and the Belt and Road Initiative and data analysis.

")