1. Introduction

The COVID-19 pandemic has brought extreme stress to the global economy. Governments around the world are trying solutions to tackle the economic crisis through various fiscal, monetary, and related stimulus packages. Policymakers are struggling to balance their stimulus between the immediate “rescue” phase and the longer-term “recovery” phase: the former is to keep businesses afloat, to provide relief for households, and preserve jobs, while the latter is to boost economic growth and transformation in the long-run. Some governments are struggling even to fulfill their current spending requirements due to their increasing public debt burdens; other forward-looking ones are particularly focused on including environmental considerations into all or some of their stimulus packages for a green recovery – that is, “an orderly transition to a more sustainable economy and climate-resilient financial system.”

To better understand the green recovery in the Belt and Road Initiative (BRI) countries, this article first explains the rationale for a green recovery, then gives an overview of the green fiscal, monetary, and prudential measures being currently implemented or planned in six BRI countries[1], representing medium/low, medium and high income groups. Finally, the article concludes with policy recommendations for each income group.

2. Rationale for a green recovery

Many countries are considering how to accelerate their recovery to set up their economies for future growth in alignment with the overall sustainable development goals (SDGs) under the motto “build back better”. A focus on green recovery can contribute to this goal due to three aspects: first, green sectors offer significant opportunities for job creation; second, green recovery measures deliver long-term economic benefits; third, green investments now reduce climate risks in the financial system and the real economy in the future.

Job creation

Green industries and activities, such as clean energy infrastructure, energy efficiency retrofits, and biodiversity conservation, create immediate and often significantly more job opportunities than the fossil fuel sectors. For example, a study using the input-output model estimates that every US$1 million spending creates 7.49 jobs in renewables, or 7.72[2] in energy efficiency, in comparison to 2.65 in fossil fuels. Thus, spending for green energy creates three times the jobs compared to spending on fossil fuels.

Furthermore, jobs in green sector are more future proof, as compared to jobs in the fossil fuel sectors: more than 1.2 million jobs in the fossil fuel industries are lost or at risk[3], while, in contrast, the energy efficiency sector alone can provide up to 2.5 million new jobs per year globally, according to the International Energy Agency (IEA).[4]

A further advantage of green recovery, particularly in energy, is that many projects in solar and wind energy, can be “shovel-ready” and able to boost job demands more imminently, while the job creation is more easily scalable with the scalability of the renewable energy projects (as compared to many fossil fuel projects).

Long-term economic benefits

On top of the immediate job creation, the long-term economic benefits are also promising in some types of clean energy infrastructure, green R&D[5], and natural capital investment. For example, among fossil fuel and renewable energy sources, geothermal and wind power plants generate the highest net GDP increases and induce the highest household incomes from the same 1GW power plant capacity investment, potentially through the multiply effect on the domestic manufacturing sector, according to a comparison study in Indonesia. Similarly, ecosystem restoration in the U.S. generates US$9.5 billion in annual economic output and US$15 billion in household spending, in addition to 126,000 direct and 95,000 indirect job creation.[6]Indeed, green measures can deliver pronounced long-term opportunities and benefits directly and indirectly to the whole economy.

Reduction of climate risks

Climate risks, if unaddressed, might bring higher costs to all sectors: each year of delay in mitigation incurs an additional 0.3- 0.9 trillion US dollars in order to meet the 2°C Paris Agreement target. This is partly driven by increasing physical risks for the financial sector and the real economy, for example, when extreme weathers and catastrophic climate events become more frequent and intense. Should policy makers accelerate changes to, for example, outlaw non-green investments or price carbon emissions (e.g., through an emission trading system), investors face additional transition risks, including the risk of stranded assets. As a result, any investments in “dirty” sectors exacerbate these risks for the financial market and the whole economy.

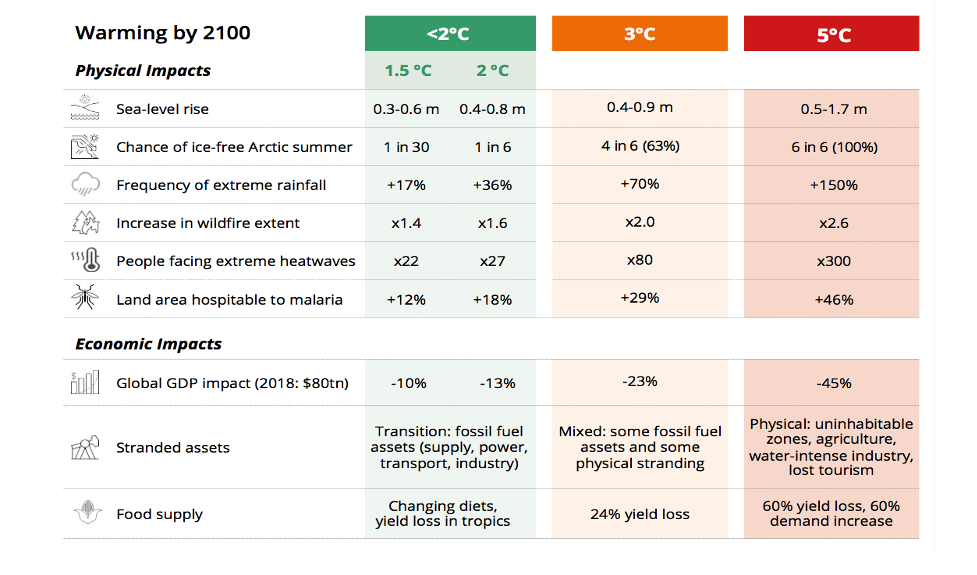

Studies found that climate adaptation costs will increase drastically in the second half of the century, without mitigation efforts; they also estimated the mitigation costs to be 1% to 3% of global GDP for a medium to likely chance of achieving the maximum temperature increase of 2°C. This compares to a potential GDP loss of more than 13% by the year 2100 if temperature changes are above 2°C, including relevant food supply loss, and 27 to 300 times the number of people facing extreme heat waves (see Figure 1). Compared to a 4°C degree warming, a 2°C warming represents avoided losses of approximately US$ 17 billion per year in the long run. Among all countries, southeast Asia (ASEAN) countries, who are extremely vulnerable to physical risks, would benefit the most from a well-below 2°C scenario.

Source: The CRO Forum, “The Heat Is on – Insurability and Resilience in a Changing Climate,” 2019

3. Green recovery in the BRI countries

To assess the opportunities and potential gaps for green recovery in BRI countries, first, it is crucial to differentiate between development stages of BRI countries: BRI countries encompass high-income, upper-middle income and lower-middle income countries. Second, it is important to learn from exemplary recovery cases. Accordingly, in this article, six BRI countries (Pakistan, Vietnam, China, Thailand, Poland and South Korea) were selected for analysis, which scored high on greenness[7] of their recovery by the Global Recovery Observatory, one of the most comprehensive green recovery database compiled and periodically updated by the University of Oxford. The six BRI countries represent different income groups: lower-middle income, upper-middle income and high income countries. Table 1 provides an overview of the six countries’ green fiscal, monetary, prudential and other related policy instruments. To better understand the recovery along its full timeline, this table also includes instruments (e.g., green taxonomy, green agenda and initiatives) that are most impactful in a medium-to-long run.

Table 1 Overview of 6 BRI countries green recovery measures

| Country income group[8] | Lower-middle income | Upper-middle income | High income | ||||

| Policy category | Policy instrument\country | Pakistan | Vietnam | China | Thailand | Poland | South Korea |

| Fiscal | Government investment | Fund 65,000 jobs for afforestation project;National park expansion;Grants for project under Sustainable Goals Achievement Program | Pollution prevention spending; Construction of rural water conservancy infrastructure; Forestry/grassland spending; Reservoir renovation;Wetland conservation and restoration; Creation of National Green Development Fund | Air quality investments | Eco-friendly manufacturing investment; Low-carbon energy investment – smart grids & renewables & eco-friendly vehicles;Zero-energy buildings;Restoring terrestrial, marine and urban ecosystems;Clean and Safe Water;Green Industrial Complexes; Green Innovation | ||

| Tax incentives | Extension of EV purchase tax exemptions; | EV investment incentives | |||||

| Subsidies & Feed-in tariffs | New feed-in tariffs for solar projects | Renewable energy subsidies (solar, wind, biomass);EV subsidies | Extension of Green Public Transport program;EV subsidies;Taxi electrification support; EV charging infrastructure; EV business purchase subsidies; Anti-smog and energy efficiency program; Support to high-efficiency cogeneration | Energy-efficient home appliances partial refunds; | |||

| Debt swaps | A debt-for-nature swap (under negotiation) | ||||||

| Issuance of sovereign green, social, and sustainability (GSS) bonds | USD $500 million green bond issuance (planned) | THB 30 billion (USD $980) Sustainability Bond | |||||

| Monetary | Collateral frameworks | PBOC accepts green bonds and green credits as eligible collateral for its lending facilities | |||||

| Prudential & others | Climate-related micro- and macro-prudential | PBOC is considering climate-related stress testing | |||||

| Green agenda and initiatives | Bank of Thailand signed MoU with UK government to develop a sustainable financial sector | ||||||

| Green taxonomy | Green Bond Endorsed Projects Catalogue (2021 Edition) |

Note: this table only covers green recovery policies during the COVID, and is not intended to be exhaustive

The overview reveals that the two lower-middle income countries prioritize nature restoration and pollution prevention in its fiscal stimulus. For example, Pakistan accelerates its afforestation projects and national park expansion. Pakistan is also aiming to reduce its debt in a green way by engaging in negotiations with its bilateral creditors, including UK, Germany, Italy and Canada, for a debt-for-nature swap.[9] Vietnam, on the other hand, provides policy instruments to accelerate renewable energy development by setting new feed-in tariffs for solar projects.

The two upper-middle income countries, in addition to nature infrastructure and pollution prevention, allocate more of their government spending on renewable energy, as well as Electric Vehicle (EV) subsidies. This also includes tax incentives for either consumption, production or investment in EVs.

The two high income countries have developed a more complete and diverse target sectors for fiscal measures. Besides fiscal support on nature conservation, pollution prevention and renewable energy, they expand their government spending to green R&D, building retrofits and energy efficiency: For example, South Korea will invest KRW 2.7 trillion (USD$2.24 billion) in green innovation and KRW 6.2 trillion (USD$5.15 billion) in building retrofit by 2025. Similar to the upper-middle income countries, they also provide subsidies for low-carbon vehicles and clean transportation infrastructure.

To mobilize private capital, sovereign green, social, and sustainability bonds are gaining traction in BRI countries. Following high income countries such as Poland and South Korea’s issuance of sovereign thematic bonds in earlier years, their lower-income counterparties — Pakistan and Thailand have raised or planned to raise more capital through “use-of-proceeds” green bond or performance-based sustainability-linked bonds to fund their green and inclusive recovery.

In summary, lower-middle income countries focus on investing in nature-related projects to create jobs, while upper-middle and high income countries have developed a green recovery through a broader suite of fiscal instruments (e.g., tax incentives and subsidies) and targeted sectors (e.g., EVs, building retrofits, energy efficiency).

4. Policy recommendations for BRI countries

For lower-middle income countries, fiscal policymakers should still prioritize nature restoration and pollution prevention projects, which are usually “shovel-ready” and able to create jobs immediately with minimal labor skill requirements. The highly-indebted countries can further negotiate debt-for-climate/nature swaps to free up the fiscal space. Additionally, low-income countries can mobilize private capital to fund clean energy and clean transport public infrastructure projects through sovereign green, social, and sustainability bond issuance (potentially with technical support from development finance institutions).

For upper-middle and high income countries, fiscal policymakers in addition to short-term measures can utilize the opportunity to invest more on green R&D, which may have a less short-term, but more long-term impacts on the economy.

To support long-term greening of the economy, financial regulators and supervisors in all countries,regardless of income levels, should guide banks, insurance companies, asset owners and asset managers to assess (i.e., climate-related stress test) and disclose (TCFD-aligned) climate-related financial risks in their lending, underwriting, and investment portfolios. Acting on climate now rather than later will prepare the financial institutions and the real economy away from another “tragedy of the horizon”. On the opportunity side, central banks and other financial regulators could also leverage their roles to encourage green lending and foster the green bond market through extending their eligible collaterals and operationalizing a green taxonomy.

[1] Lower-middle income countries: Pakistan, Vietnam; Upper-middle income: China, Thailand; High-income: Poland, South Korea

[2] 9-30 jobs per million USD spending in energy efficiency, according to International Energy Agency (IEA), “Sustainable Recovery,” 2020.

[3] International Energy Agency (IEA), “Sustainable Recovery.”

[4] IEA data cited in OECD, “Making the Green Recovery Work for Jobs, Income and Growth,” October 6, 2020.

[5] Cameron Hepburn et al., “Will COVID-19 Fiscal Recovery Packages Accelerate or Retard Progress on Climate Change?,” Working Paper No. 20 02 ISSN 2732 4214 (Online) (Oxford Smith School of Enterprise and the Environment, May 4, 2020).

[6] BenDor et al., “Estimating the Size and Impact of the Ecological Restoration Economy.” cited in OECD, “Biodiversity and the Economic Response to COVID-19: Ensuring a Green and Resilient Recovery.”

[7] The greener, the more positive impact on net GHG reduction, vice versa.

[8] World Bank classification

[9] “Pakistan Nears Debt-for-Nature Swap Agreement with Creditors.”

Thumbnail photo credit: The third wave – Graeme Mackay

Yingzhi Sarah TANG is a non-resident fellow at the Green Finance & Development Center. She previously served as Deputy Director for the Green BRI Center at International Institute of Green Finance in Beijing.

She has been leading projects in close collaboration with both Chinese and international partners to better understand the latest development of Chinese overseas investment along the BRI, including policies, strategies and innovative green finance instruments.

Before joining the teams in China, Sarah has worked on insurance and banking sectors’ climate risk assessment projects at UNEP Finance Initiative (Switzerland) and the Intact Centre on Climate Adaptation (Canada).

She holds a research-based Master’s degree in Environmental Studies (Sustainability Management) from University of Waterloo, Canada, and double Bachelor’s degrees in Environmental Studies and Business Administration from both Canada and China.

Dr. Christoph NEDOPIL WANG is the Founding Director of the Green Finance & Development Center and a Visiting Professor at the Fanhai International School of Finance (FISF) at Fudan University in Shanghai, China. He is also a Professor at The University of Queensland and the lead for Asia Pacific Industry Transitions.

Christoph is a member of the Belt and Road Initiative Green Coalition (BRIGC) of the Chinese Ministry of Ecology and Environment. He has contributed to policies and provided research/consulting amongst others for the China Council for International Cooperation on Environment and Development (CCICED), the Ministry of Commerce, various private and multilateral finance institutions (e.g. ADB, IFC, as well as multilateral institutions (e.g. UNDP, UNESCAP) and international governments.

Christoph holds a master of engineering from the Technical University Berlin, a master of public administration from Harvard Kennedy School, as well as a PhD in Economics. He has extensive experience in finance, sustainability, innovation, and infrastructure, having worked for the International Finance Corporation (IFC) for almost 10 years and being a Director for the Sino-German Sustainable Transport Project with the German Cooperation Agency GIZ in Beijing.

He has authored books, articles and reports, including UNDP's SDG Finance Taxonomy, IFC's “Navigating through Crises” and “Corporate Governance - Handbook for Board Directors”, and multiple academic papers on capital flows, sustainability and international development.

")