Executive summary

In March 2026, during the so called “Two Sessions”, China agreed on its 15th Five-Year Plan (FYP) (the draft had been circulated since October 2025) as a follow up to the 14th FYP (for a comparison of the major targets between the 14th FYP and 15th FYP, see Appendix). As the major policy document determining China’s development for the period from 2026 to 2030, the FYP significantly impacts and drives China’s green development outcomes:

- The lack of absolute emission reduction targets in the 15th FYP is consistent with China’s green development ambitions and policy. While several analyses (eg here or here) have noted the lack of ambition in emission reduction by providing neither more ambitious emission intensity target (which was 18% reduction in the 14th FYP and is 17% in the 15th FYP) or by providing absolute emission reduction target to accelerate China’s green development, this was not an accidental lack. Rather it is aligned with China’s policy trajectory. Importantly, the move to “dual control of carbon” including absolute carbon emission control is deeply anchored in the 15th FYP.

- China’s emission trajectory based on 15th FYP targets would not allow for a carbon peaking before 2030 (a requirement to meet China’s policy to peak carbon emissions before 2030).

- China’s goals for non-fossil energy additions would see China’s annual green energy additions fall by more than half compared to the 14th FYP.

- At the same time, fossil fuel energy consumption would increase by 8-10%, reversing the slow-down in fossil fuel energy consumption during the 14th FYP period.

- Contrary, if the trajectories of the past 5 years of non-fossil energy consumption growth would prevail, China would continue to fully satisfy its growing energy demand through renewable energy.

- Industrial decarbonization goals are lacking ambition focusing only on minor adjustments to locate production facilities into regions with significant renewable energy resources, as well as to establish new green industrial zones.

- China aims to expand its global green technology leadership covering areas like green energy generation, new types of batteries and significant expansion of green hydrogen. The latter two technologies made it into the top 10 of China’s new industries (amongst other future tech like integrated circuits and low-altitude equipment).

What to watch for decision-makers: The 15th FYP is a high-level planning document. It shows significant ambitions on some aspects but is more a guidance document – including for green growth. More important will be the different policies, regulations and guidances of line ministries and provinces as well as the annual government work plan that fill the FYP with life and detail. As one example, China, on March 12, passed the Environmental and Ecological Code, codifying over 30 laws into a single umbrella, combining pollution control, ecological protection and climate action.

The following sections provide comprehensive analyses and simulations of the possible impacts of the 15th FYP covering climate emissions, green energy generation, battery energy storage, green hydrogen, fossil fuels, industrial decarbonization, and green finance. Each section also provides a short overview based on data analyses of China’s development trajectory over the past years.

Climate emission

Status of climate emissions

China’s emission targets are mostly defined by its climate goals to peak emissions before 2030 and become climate neutral by 2060 (which is also anchored in policy since 2021). This policy leaves room for China to grow emissions until 2030 – albeit that would make China’s emission reduction to net zero by 2060 more challenging.

Thus, rather than having absolute emission reduction targets, China has operated with relative targets to reduce emission intensity the five-year plans (i.e., emissions per unit of GDP). The 14th FYP, for example, had a binding target of 18% reduction of emission intensity. As I had previously analyzed, this goal would see China’s absolute emissions grow by 5% and peak in 2027 at a 5% GDP growth rate.

Considering, China’s economy grew by an average of only 4.54% in the 14th FYP according to data from China’s statistical yearbook (rather than 5% assumed in earlier calculations), China reported an absolute emission reduction in energy and industry of 0.3% in 2025 and the a reduction of 17.7% emission intensity reduction between 2020 and 2025. CREA’s analyses posits that this reduction was possible due to changes in the calculation methodology, in particularly by expanding the scope from energy-related emissions to non-energy related emissions.

What to expect from the 15th FYP regarding climate emissions

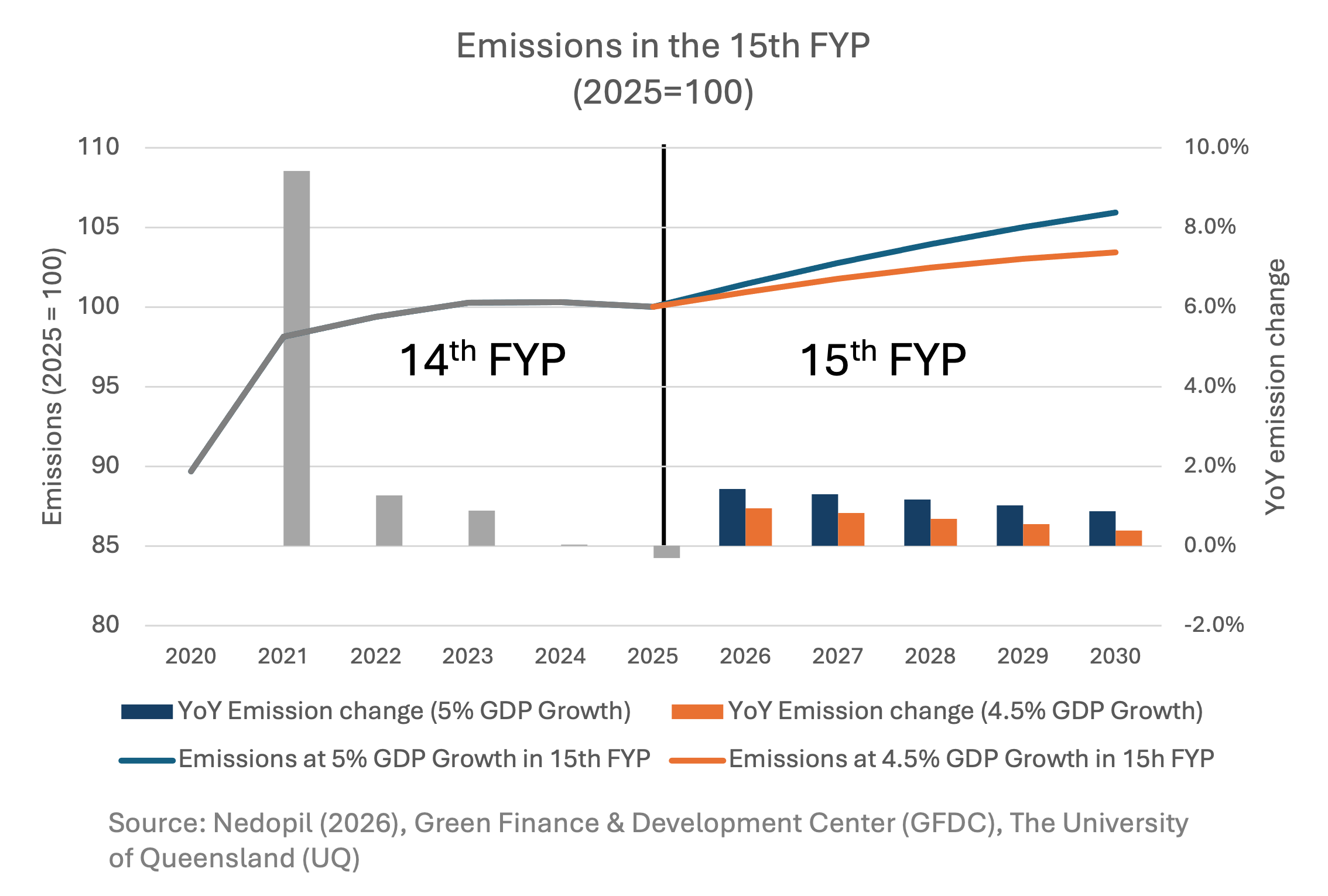

Looking to the next 5 years with an expected GDP growth rate of 4.5% to 5% and the 17.7% reduction target for emission intensity, absolute emissions could rise by 3% to 6% by 2030. It is also noteworthy that this trajectory would not allow for China to peak emissions before 2030.

However, considering current emission trajectories and a continuous ambition in green energy deployment, it is possible for China to overperform with a resulting flat line or even reduction of emissions. This, as will be discussed in the next section, is due to weak green energy growth targets anchored in the 15th FYP – which seem easy to overachieve.

Some outside observers had also expressed disappointment that the 15th FYP would offer an absolute emission reduction target. This hope may have been fuelled by China’s announcement in September 2025 to reduce absolute greenhouse gas emissions by 7 to 10% from peak levels by 2035.5 Yet, Chinese government was clear in its ambitions to move from “dual control system” (i.e., control of energy intensity and energy consumption) to “dual carbon control” (i.e., control of carbon intensity and absolute carbon emissions) during the 15th FYP rather than at the launch of the 15th FYP in various policy documents.

Accordingly, the 15th FYP anchors that the dual control of total carbon emissions and intensity needs to be implemented during the 15th FYP period. This also includes the further improvement of the national carbon emission data comprehensive management system and the national greenhouse gas emission factor database.

Green energy generation

Status of green energy generation

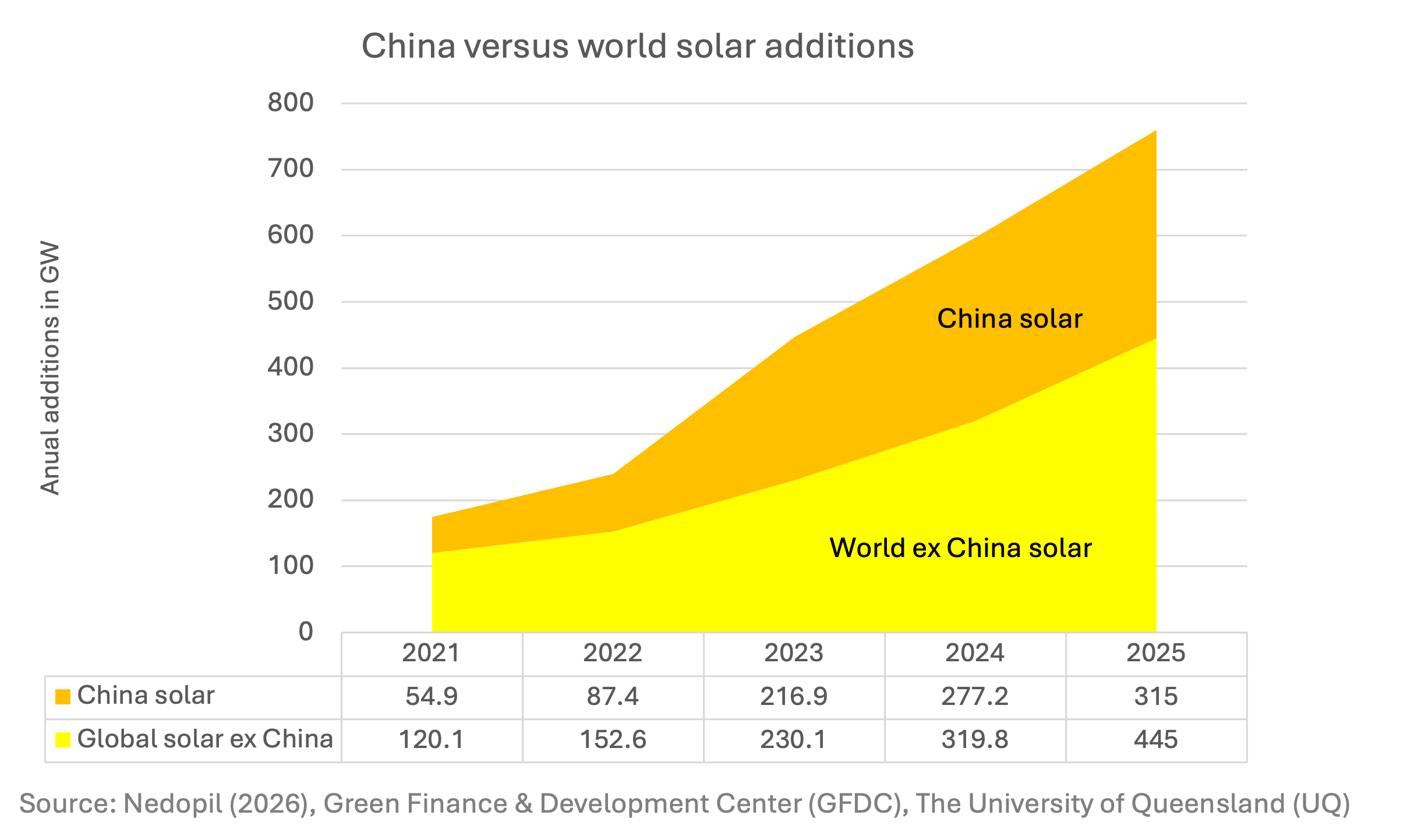

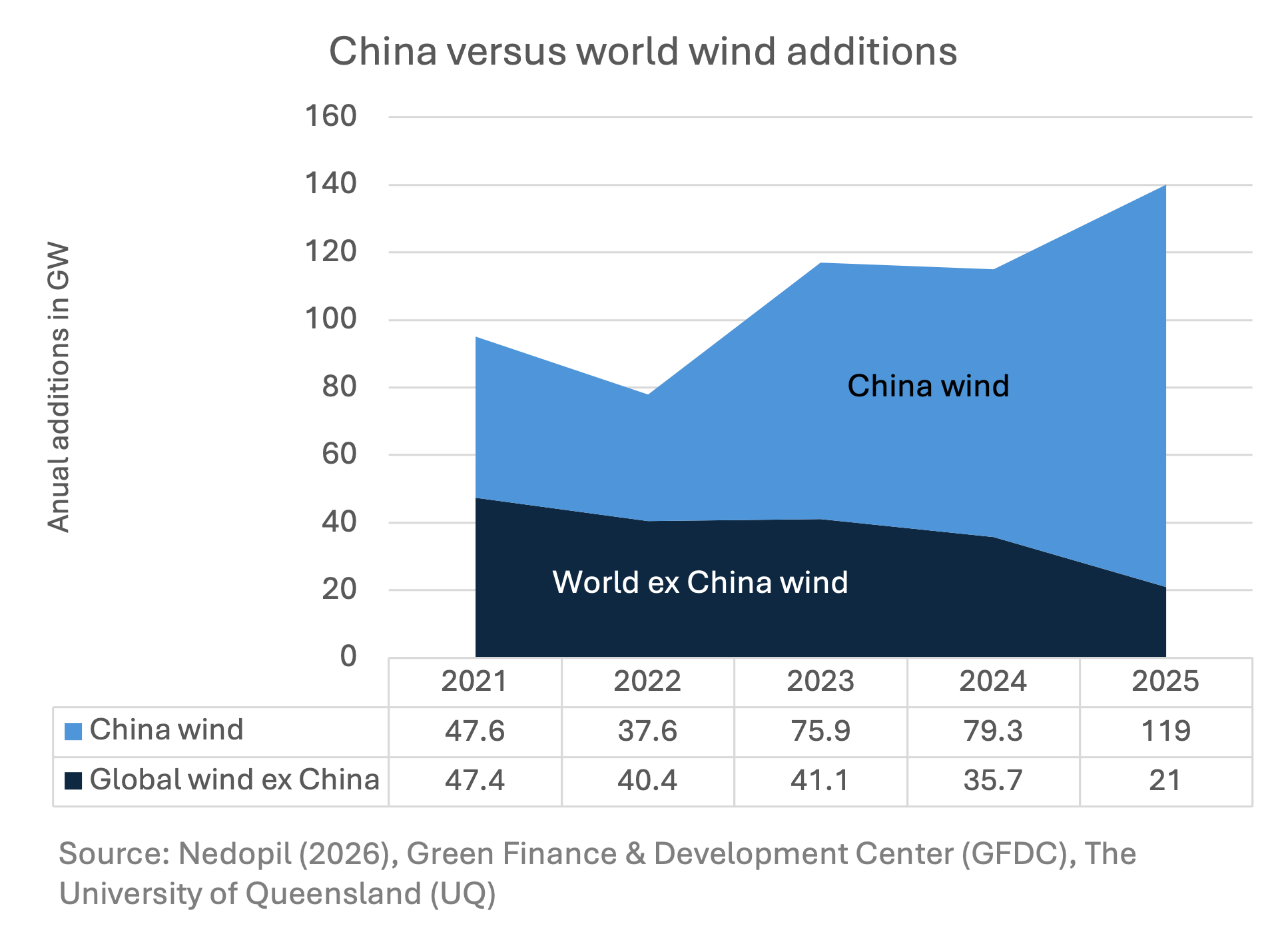

During the 14th FYP (i.e., from 2021 to 2025), China added about 951 GW of solar and 359 GW of wind capacity. China’s solar/wind additions account for about 43% and 66%, respectively, of global installations (see Figure 2a and 2b).

During that time, China’s green energy share increased from about 16.7% in 2021 to 21.7% in 2025. In the five years, non-fossil energy consumption increased by 69%, or an average of 11% per year.

Considering the growth in total energy consumption of 24% in the past five years, this means also that fossil fuel energy consumption increased by about 10% in this period.

At the same time, China missed its energy intensity target of 13.5% and only achieved a reduction of about 1.6%.

What to expect from the 15th FYP for green energy generation

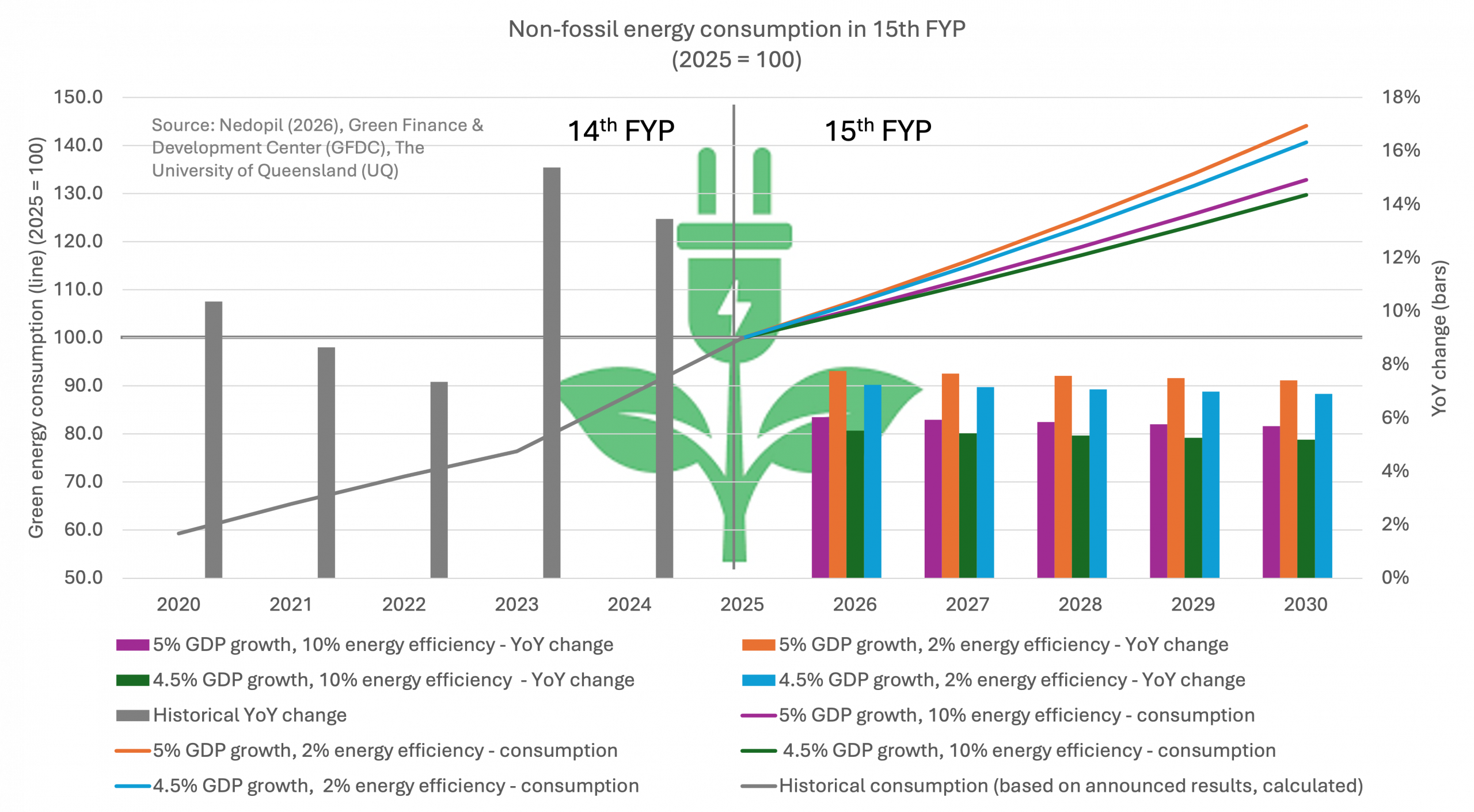

A few goals related to energy have been announced in the 15th FYP that allow to calculate non-fossil fuel energy and fossil-energy growth: 10% energy intensity reduction goal and a 25% share of non-fossil energy by 2030.

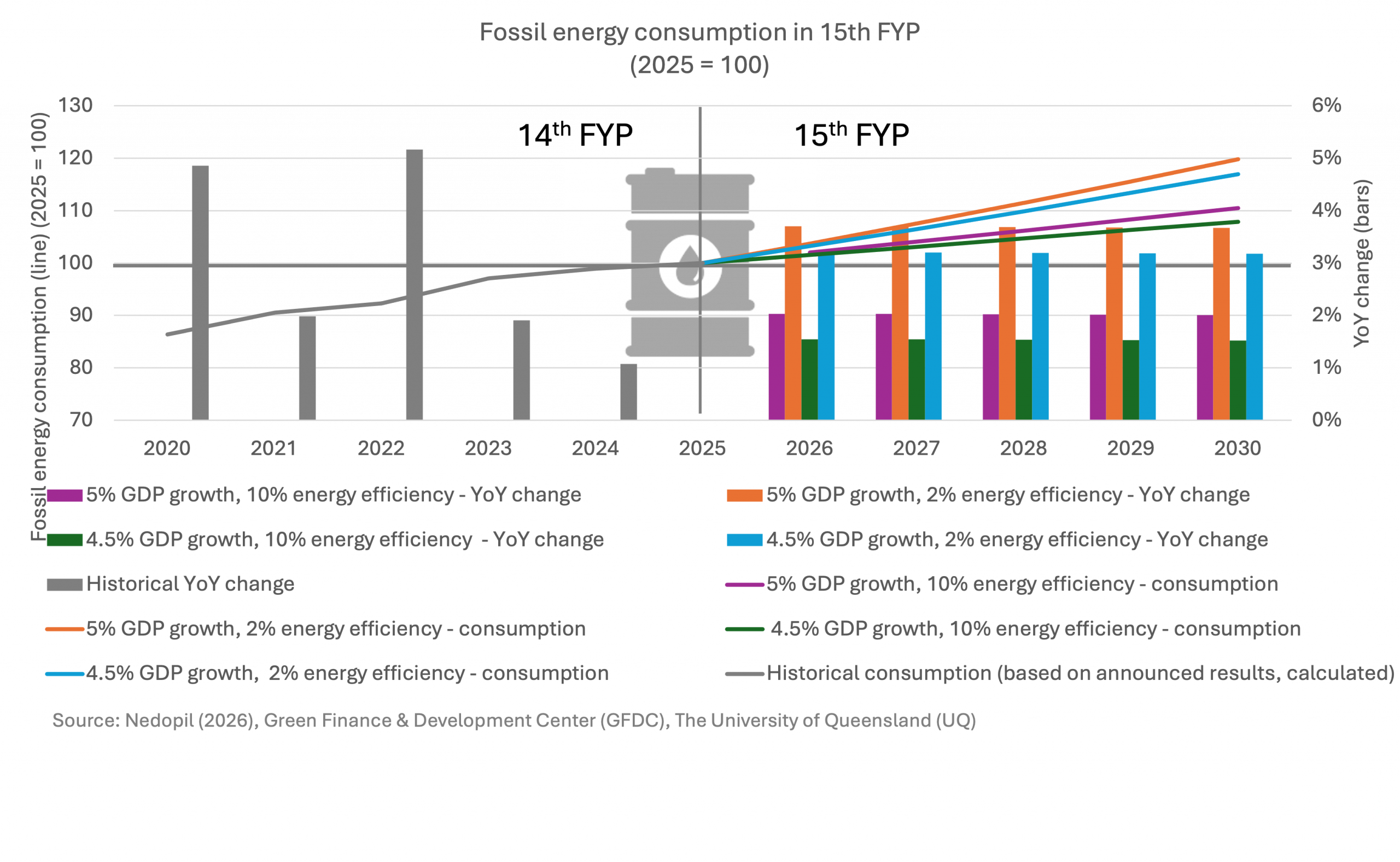

Achieving these goals under a 4.5% to 5% annual GDP growth scenarios would require non-fossil fuel energy growth of about 29.8% to 32.9% by 2030. This equals to about 5.9% non-fossil energy consumption growth per year. This is significantly lower than the 11% average in the 14th FYP or 15% and 14% green energy consumption growth in 2024 and 2025, respectively (see Figure 3).

For fossil fuel consumption, these targets would mean an increase of consumption by 7.9% to 10.5% in 2030 (see Figure 4). Considering the better economics of green energy versus fossil fuels, this seems a non-sensible pathway for China. This development is also significantly above the fossil fuel energy addition trend of the 14th FYP period.

Conversely, the 15th FYP highlights ambitions to “advance safe, reliable, and orderly substitution of fossil energy with non-fossil energy” while advancing diverse energy development “with wind, solar, hydro and nuclear power as the main focus”.

Throughout all simulations, it is also important to consider that the 13.5% energy intensity reduction target of the 14th FYP was not met. Accordingly, to understand the potential impact of higher energy needs to drive economic growth driven by the expansion of energy intensity sectors (e.g., data centres), the simulations also include a scenario where China achieves only a 2% energy intensity reduction target in the 15th FYP. As seen above in the two figures, China would need to increase non-fossil fuel energy consumption by 40 to 44% and fossil fuel energy consumption by 17 to 20% with a GDP growth of 4.5% to 5% per year.

For China to achieve no additions in fossil fuel consumption, it would need to increase its non-fossil fuel energy consumption share to between 30.5% and 37.4% in 2030, depending on the GDP growth and energy intensity achievements (see Table 1). Factually, this would mean that China would need to continue its expansion of non-fossil fuel energy like rates achieved during the 14th FYP. Under this circumstance, China would triple its non-fossil fuel energy consumption from 2021 to 2030.

Table 1: Non-fossil fuel share for 0 percent fossil fuel consumption change

| GDP growth Energy intensity reduction | 4.5% | 5% |

| 2% | Non-fossil fuel share in 2030: 35.9% Average annual growth: 15.1% | Non-fossil fuel share in 2030: 37.4% Average annual growth: 16.6% |

| 10% | Non-fossil fuel share in 2030: 30.5% Average annual growth: 9.6% | Non-fossil fuel share in 2030: 32.1% Average annual growth: 11.3% |

Battery energy storage

Status of battery energy storage

Battery energy storage (BES) is a core component of a renewable energy system to allow for intermittency of solar and wind energy generation by storing energy surplus and releasing it in high-demand or low renewable energy generation periods. To this end, China had installed 145 GW of battery storage by the end of 2025. 60 GW of this was added in 2025 alone. China exerts significant control of the battery market, producing about 69% of cells, 80% of lithium-ion batteries and 90% of graphite.

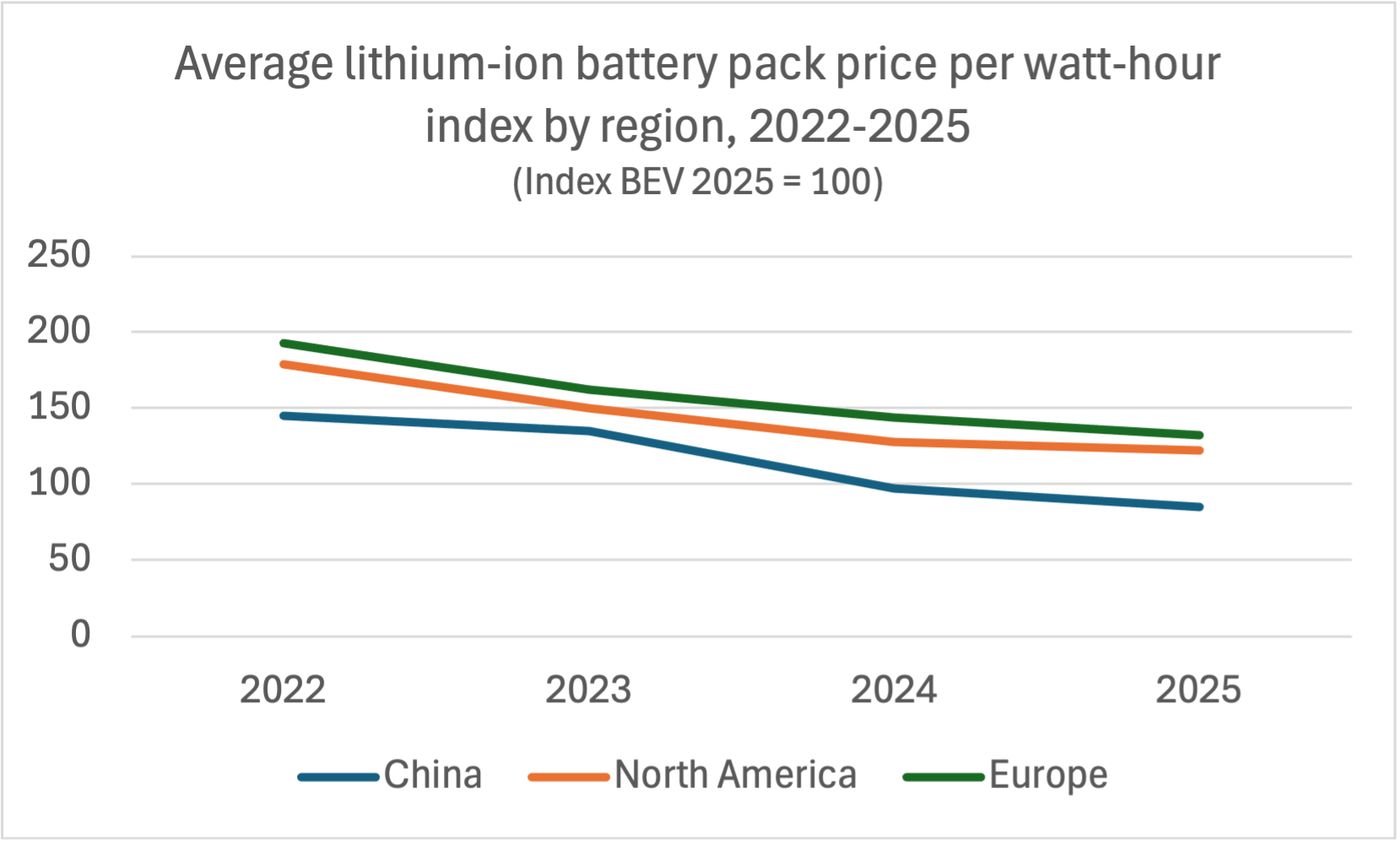

What was also significant was China’s rapid drop in per MWh cost outpacing the rest of the world by more than 30% over the past 2 years, as calculated by IEA (see Figure 5).

What to expect from the 15th FYP for battery energy storage

The 15th FYP highlights further strengthens China’s ambitions in BES. New-type batteries are one of the 10 core new innovations. Specifically, China aims to “accelerate the breakthrough of key materials such as high-capacity electrode materials, high-conductivity electrolyte materials, and composite current collectors, develop high-precision coating and high-speed stacking high-end manufacturing equipment and processes, expand applications of high-safety and high-energy-density batteries in new intelligent terminals, new energy storage, electric transportation vehicles, and other domains“.

Green hydrogen

Status of green hydrogen

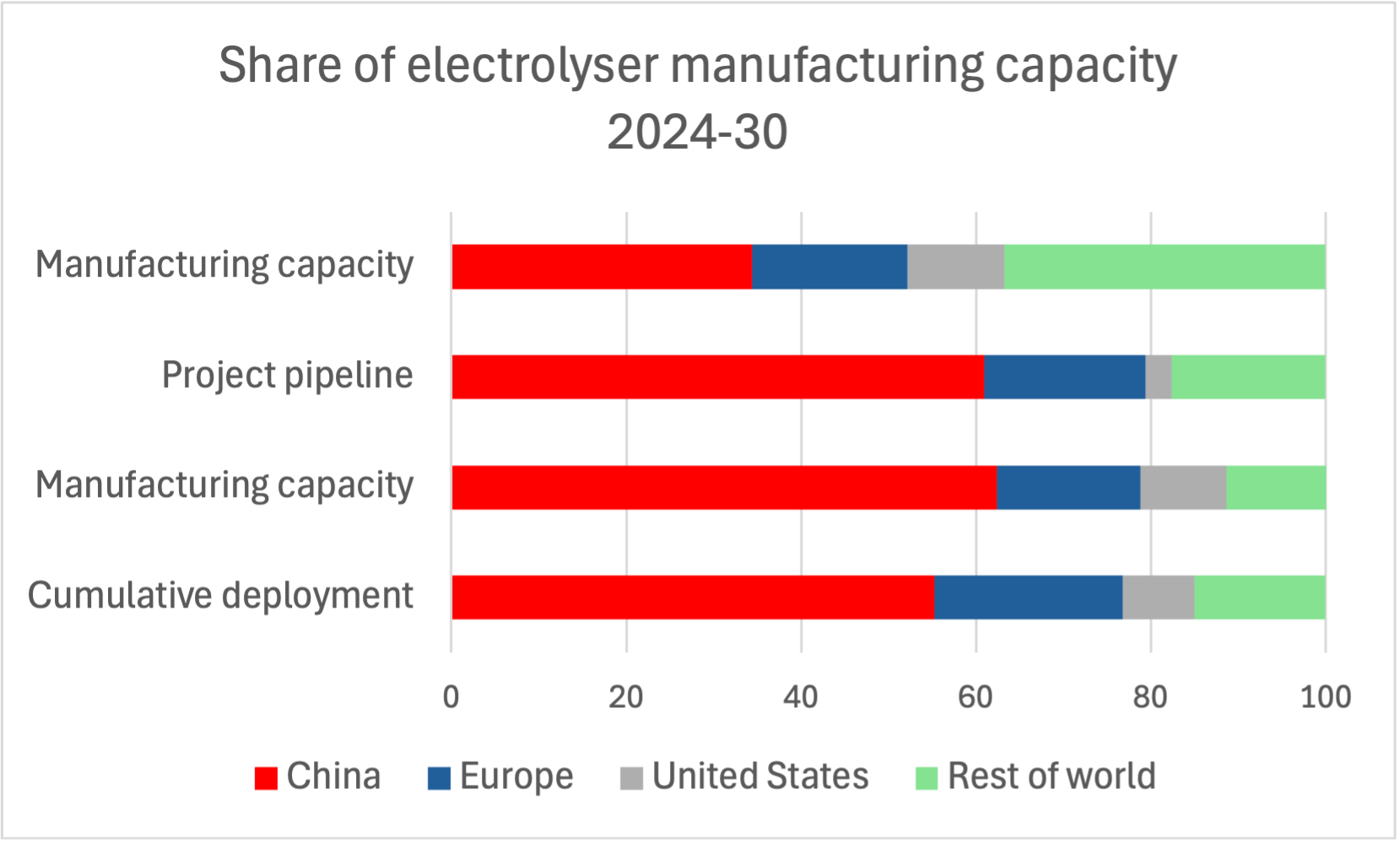

China controls an estimated 60 per cent of global electrolyser capacity and can produce green hydrogen at a cost of approximately $3.70 – $5.20 per kilogram—up to 50 per cent cheaper than in Western markets. Part of this success is the relatively fast growth of new capacity, where in 2024, China added more than 60 per cent of the 70,000 tonnes of global annual capacity. In 2025, orders for electrolysers were expected to double compared to 2024, to more than 5 GW, with an additional 7 GW of EPC projects. The country is also developing legal guidelines for the transport of hydrogen developed by various ministries in 2025. A landmark guideline was published in October by China’s leading ministry, the National Development and Reform Commission (NDRC), which expanded funding for green hydrogen and its industrial applications eligible for national grants, seen by some as the first national funding mechanism for hydrogen-adjacent technologies. Also, the 2026 Government workplan has put forward a new national fund to foster new growth drivers such as hydrogen power and green fuels.

What to expect from the 15th FYP for green hydrogen

The 15th FYP puts forward a very strong case to extend the development and use of green hydrogen. Green hydrogen is one of the 10 core new industry levers. Specifically, the plan lays out the ambition to improve the level of renewable energy hydrogen production equipment, accelerate technological breakthroughs and verification of economical and safe scaled hydrogen storage and transportation, optimize the layout of hydrogen energy infrastructure, advance the hydrogen energy industry chain toward green ammonia, methanol, and sustainable aviation fuels, expand applications of hydrogen energy in transportation, electricity, industrial, and other domains.

The 15th FYP further lays out the ambition to build hydrogen refuelling stations for transport, alongside battery swapping, ammonia, and methanol refuelling.

Overall, the IEA expects that China’s green hydrogen production will grow five-fold in the next five years with China controlling significant stakes of the hydrogen supply chain (see Figure 6).

Fossil fuels

Status of fossil fuels

China remains the world’s dominant consumer and importer of fossil fuels. Fossil fuels are used for a variety of purposes (see Table 2). It uses 56% of global coal, 15% of global oil (second largest after the USA), and about 9-10% of global gas. Significant portions of the fuels are imported – with numbers ranging from 72% for oil, 61% of gas and 10% of coal.

China’s fossil fuel strategy is shifting toward “energy security” by maximizing domestic output alongside its green transition. Over the past years, China has increased its domestic capacity to source and process fossil fuels to mitigate geopolitical risks – including for Coal-to-Chemicals(“coal-to-liquids” and “coal-to-gas”) projects to convert its abundant coal into transport fuels and industrial feedstocks. China has also built the world’s largest oil refining capacity, shifting from importing refined products to exporting. The security concerns in fossil fuels also touches upon food security with China’s domineering role in global fertilizer production.

Table 2: The role of fossil fuels in China

| Fuel Type | Global Consumption Share | Import Dependency | Use | Key Strategic Trend |

| Coal | ~56% (World’s largest) | ~10% (World’s largest importer) | Energy generation (60% of total coal use providing 51% of electricity generation) Coal-to-chemicals Metals Nitrogen production (fertilizer) | Expanding “Coal-to-Chemicals” to reduce oil reliance. |

| Oil | ~16% (World’s 2nd largest) | ~72-75% (World’s largest importer) | Transport Petrochemicals | Reaching “Peak Oil” demand due to EV penetration. |

| Natural Gas | ~9-10% | ~60% (Top 3 importer) | Urban heating Fertilizer production High-precision manufacturing (requiring heat or chemical reactions) | Increasing domestic shale and deep-sea production. |

What to expect from the 15th FYP for fossil fuels

The current energy targets of the 15th FYP see fossil fuel for energy consumption increases by about 13% (as discussed above). In addition, fossil fuel use is supported in the 15th FYP for chemical process, and in particular coal-to-oil and coal-to-gas production. Driven by its goal for energy security, the 15th FYP highlights that China will “persist in domestic self-sufficiency for core oil and gas demand, implement mid- to long-term oil and gas reserve increase and production strategic action, ensure crude oil annual production remains stable at around 200 million tons, natural gas production steadily increases”. The ambition for national self-sufficiency in energy production was also elevated to a main target with the goal to increase energy production capacity from 5.13 billion to 5.8 billion tons of standard coal.

Furthermore, the 15th FYP elevates the government’s ambition of securing the provision of grains and food security requiring fertilizer production (using fossil fuels). While China tried to reduce the use of fertilizers through several initiatives, such as “Hundred Counties” launched in 2017, China aimed to reduce use of fertilizer, the elevated gravity of grain production might expand the use of fertilizers. Possibly, China hopes to reduce use of fossil fuels in fertilizers through use of green ammonia.

In short, the 15th FYP aims to “promote the peaking of coal and petroleum consumption”.

Industrial decarbonization – metals, cement, and chemicals

Status for industrial decarbonization

Industrial decarbonization focuses on high-emission sectors, specifically metals, cement, and chemicals.

In the metals sector, where China is responsible for 51% of global steel production, 61% of pig iron, and 60% of aluminium, key decarbonization ambitions have been missed. An important target in the steel sector was a 15% share of electric arc furnace (EAF) for steelmaking – which stagnated at approximately 10-11% due to high electricity switching cost. Consequently, new plans for 2026 mandate stricter capacity swaps and the retirement of aging coal-fired blast furnaces to force a structural plateau in sectoral emissions.

Nevertheless, due to declining demand (and, possibly, the inclusion of metals and cement in the National Emissions Trading Scheme (ETS) during 2024 and 2025), the metals sector saw a 3% emission decline (see Table 3 for the breadth of metals to be considered).

Table 3: Main metals for China’s decarbonization

| Type of metal | China’s global share | Carbon emissions | Emission reduction trajectory |

| Steel | ~52% | Second largest industrial emitter; accounts for ~17% of national CO2 emissions. | Peaked/plateaued production around 2024. Extension of EAF use and control of demand. Inclusion in National ETS |

| Aluminium | ~60% | Highly electricity-intensive; historically coal-reliant but shifting to hydro-rich regions. | Plateaued production around 2024; now included in National ETS with a focus on increasing renewable energy share to 30%+. |

| Magnesium | ~90% | Extremely high intensity due to the thermal Pidgeon process; significant SF6 (GHG) usage. | Facing stricter environmental benchmarks; 2026 targets focus on retrofitting smelting plants with energy-saving vertical tanks. |

| Silicon Metal | ~75% | High heat and electricity demand for chemical reduction; critical for the solar and EV supply chain. | Transitioning to green power sourcing; emissions are decoupling from growth as low-carbon silicon becomes a trade requirement. |

| Copper | ~51% | Moderate intensity per tonne but expanding absolute production due to electrification. | Emissions reporting became mandatory in 2025/2026; focus is on secondary recycling (scrap) to lower the carbon footprint. |

| Ferroalloys | ~60% | Intense carbon footprint from chemical reduction and large-scale power consumption. | Industry consolidation is underway to phase out smaller, high-emission furnaces in favour of high-efficiency models by 2030. |

The cement sector, meanwhile, saw a 7% drop in emission in 2025, mostly due to a weak construction market.

The chemical sector remains a significant outlier with emissions rising by 12% in 2025 due to a surge in coal and oil consumption for feedstock and fuel. While it was not part of the initial ETS expansion, the government plans to integrate chemicals by 2027 to address this growth. Currently, decarbonization in this sector relies on large-scale green hydrogen pilot projects intended to replace coal-based ammonia and methanol production.

What to expect from the 15th FYP for industrial decarbonization

Industrial decarbonization is an important, albeit not central part of the 15th FYP. The plan stipulates to “significantly increase energy efficiency and carbon reduction renovation efforts in key industries and sectors such as thermal power, steel, non-ferrous metals, petrochemicals, chemicals, and building materials, promote and popularize energy-efficient and low-carbon technologies, achieve energy savings of more than 150 million tons of standard coal equivalent”. While this reduction of about 1.7 TWh in energy consumption seems large – it is insignificant considering over 400 TWh of electricity already used in the metals sector per year10.

Additionally, China aims to implement low-carbon renovation projects for coal chemical processing.

Overall, however, there is likely no additional acceleration for industrial decarbonization with a focus on “accelerating the adjustment and optimization of industrial structure“ to support carbon peaking.

Accordingly, China aims to “establish industrial carbon emission management mechanisms, clarify carbon emission management requirements for key industries and sectors, and advance production capacity governance and dual control of carbon emissions”. This means that some industrial sectors will see absolute emission targets. Furthermore, China’s aim to develop 100 green industrial parks and promote the relocation of energy intense industries to green energy rich regions will further help reduce industrial emissions.

Green finance

Status of green finance

Green finance is a core component of China’s green growth ambition that allows financial institutions to provide financing at competitive rates to companies while companies might benefit from lower financing and transaction cost when pursuing decarbonization and green growth activities.

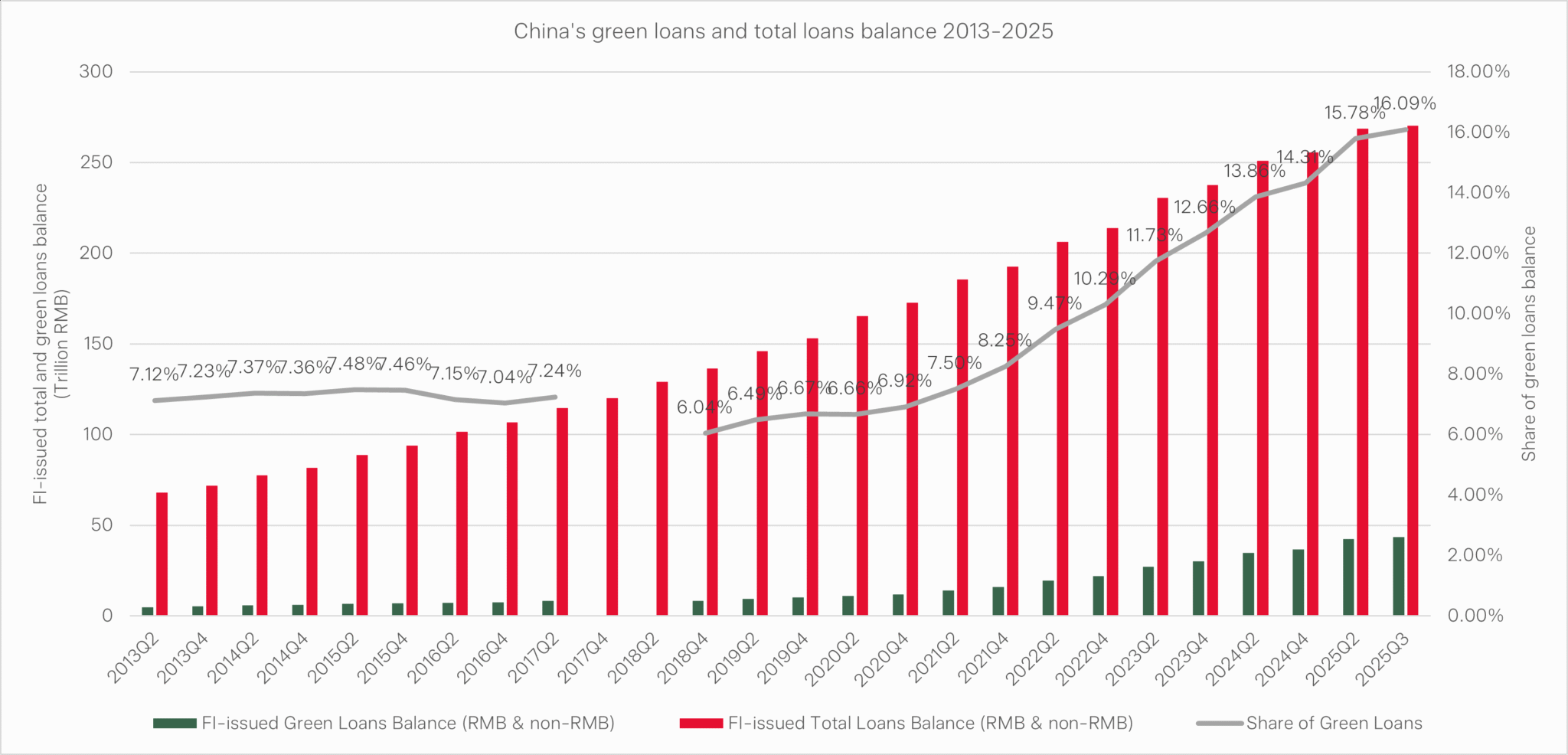

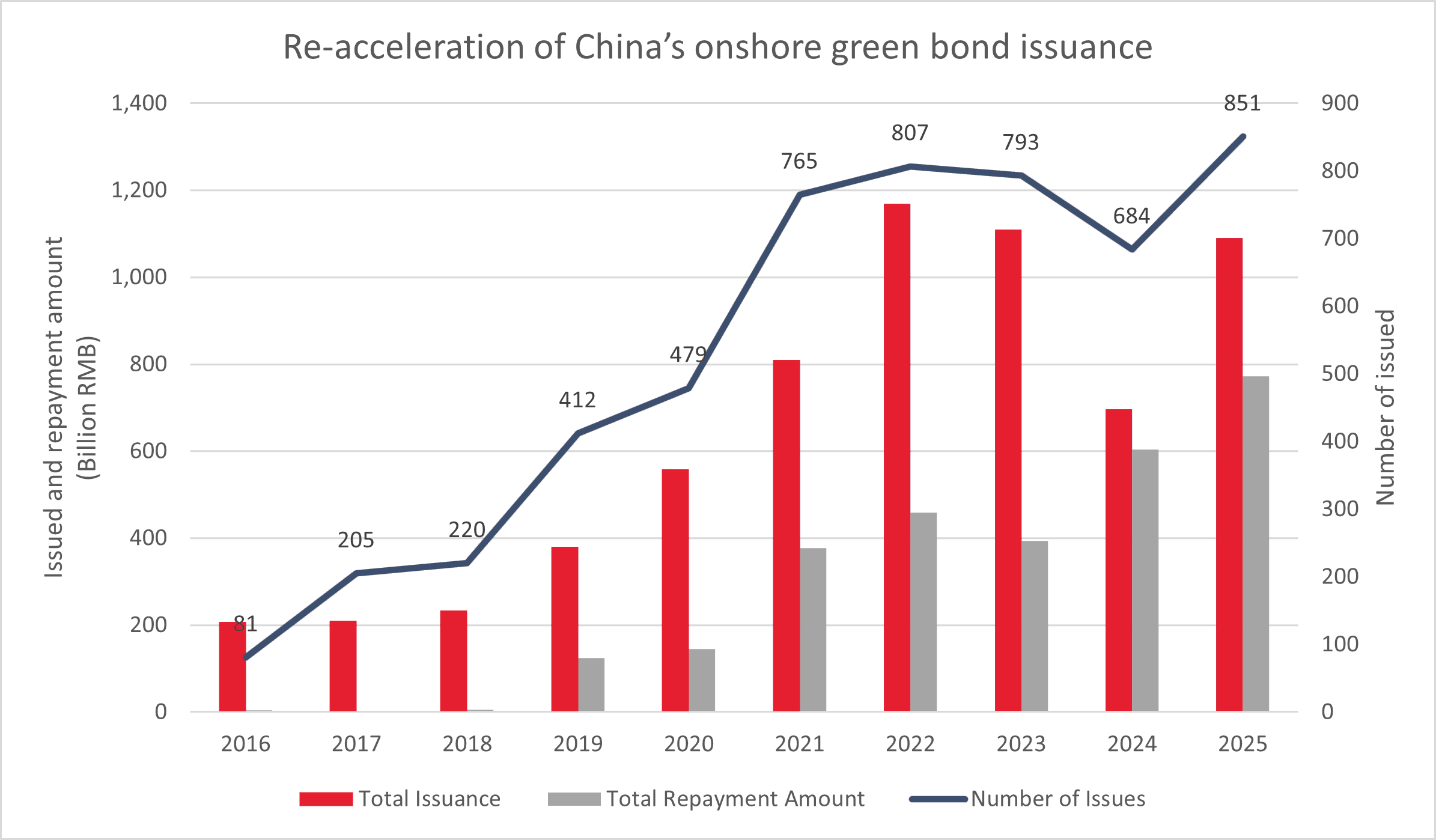

China’s green finance system has seen steady advances since its foundation in 2015. In Q3 2025, China’s green credit stood at USD6.2 trillion (up USD 0.9 trillion) and over the year 2025, it issued USD 154.7 billion in green bonds (see Figure 7a and Figure 7b).

Over the past two years, China has significantly advanced climate-related reporting for both listed and unlisted companies including Scope 1, 2 and 3 emissions as well as double materiality considerations to address both climate risks on companies as well as the risks of company activities on climate change.

What to expect from the 15th FYP for green finance

Green finance will see continued support in the 15th FYP period. Specifically, the government aims to “enrich green financial products and services, orderly advance carbon finance product and derivative tool innovation, improve the green finance evaluation system for financial institutions, and encourage the increase of investment ratio in green and low-carbon sectors.”

Also, information disclosure should be improved through “legally mandated and voluntary disclosure of enterprise climate information and environmental information”. Disclosure might thus go beyond climate related disclosure and include nature-related disclosure as well.

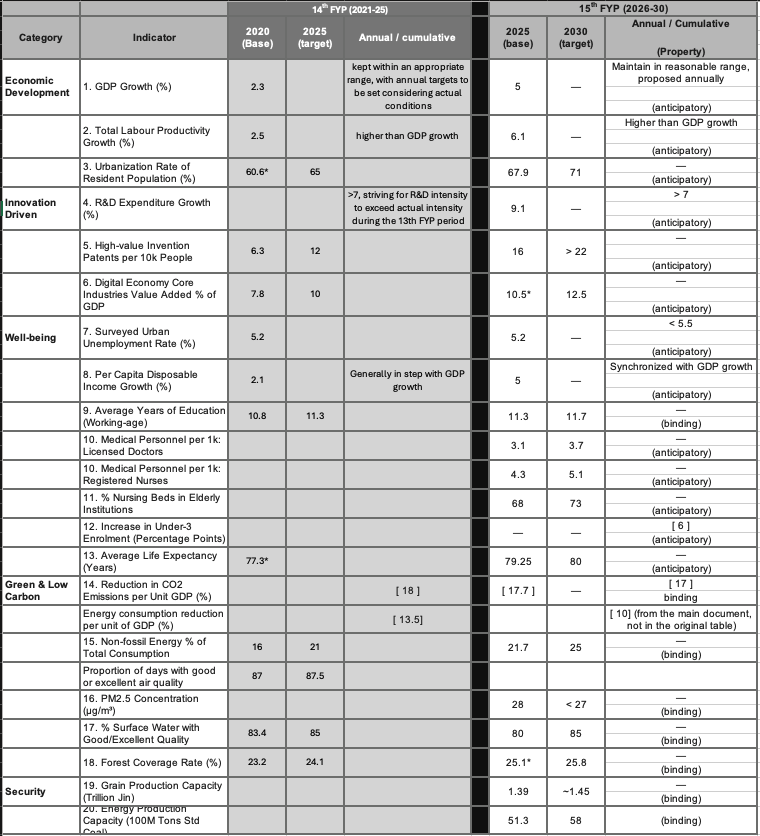

Appendix – Comparison of targets of the 14th and 15th Five-Year Plan (FYP) China

Dr. Christoph NEDOPIL WANG is the Founding Director of the Green Finance & Development Center and a Visiting Professor at the Fanhai International School of Finance (FISF) at Fudan University in Shanghai, China. He is also a Professor at The University of Queensland and the lead for Asia Pacific Industry Transitions.

Christoph was a member of the Belt and Road Initiative Green Coalition (BRIGC) of the Chinese Ministry of Ecology and Environment. He has contributed to policies and provided research/consulting amongst others for the China Council for International Cooperation on Environment and Development (CCICED), the Ministry of Commerce, various private and multilateral finance institutions (e.g. ADB, IFC, as well as multilateral institutions (e.g. UNDP, UNESCAP) and international governments.

Christoph holds a master of engineering from the Technical University Berlin, a master of public administration from Harvard Kennedy School, as well as a PhD in Economics. He has extensive experience in finance, sustainability, innovation, and infrastructure, having established the Green Belt and Road Initiative Centre at the International Institute of Green Finance (IIGF) in Beijing, having worked for the International Finance Corporation (IFC) for almost 10 years and being a Director for the Sino-German Sustainable Transport Project with the German Cooperation Agency GIZ in Beijing.

He has authored books, articles and reports, including UNDP's SDG Finance Taxonomy, IFC's “Navigating through Crises” and “Corporate Governance - Handbook for Board Directors”, and multiple academic papers on capital flows, sustainability and international development.

2026 H1")

")