This executive summary is based on the full report, “China Green Finance Status and Trends 2025-2026” by Fang Yang, Jinze Li and Christoph Nedopil, co-published with the Griffith Asia Institute. The report provides a comprehensive analysis of China’s green finance policies, market developments, and strategic recommendations to accelerate the sector’s growth.

Introduction and background

China’s green finance development in 2025 continued to make significant progress across several areas. This advancement contrasts with trends in many Western markets, which have slowed or, in the case of the United States, reversed progress on green and sustainable finance. China’s advancements in green finance appear to be driven by three factors:

- Policy trumps politics: unlike many Western countries, Chinese politics is less public, allowing policymakers to focus more on policy development. This enables the evaluation of environmental risks, such as climate change and biodiversity loss, based on scientific evidence rather than populism or current voter sentiment. As a result, policy recognises the need for green finance to address both short-term and long-term financial risks associated with climate change. This also reflects another feature of China’s system – long-term planning, in contrast to the shorter political election cycles in many Western countries.

- Green economy opportunities: China is increasingly capitalising on the economic opportunities presented by a green transition, supported by a growing green real economy (e.g., in renewable energy, electric vehicles, and green industrialisation). These opportunities manifest in green economy equipment (e.g., solar PV panels, wind turbines, batteries) as well as in the cost advantages of a green transition (e.g., lower energy prices)

- Green finance knowledge and capacity in key institutions: Key institutions, such as the People’s Bank of China (PBoC) (China’s central bank) and related government and non-government entities (both financial and non-financial), have developed strong expertise in green finance since the top-level establishment of China’s green financial system in 2015. Although significant gaps persist across the financial ecosystem, China’s green finance capacity is likely world-leading, enabling it to export its knowledge base (e.g., through the Green Investment Principles (GIP), the Global Green Finance Leadership Program (GFLP), and the Capacity Building Alliance of Sustainable Investment (CASI).

In 2025, China’s green finance development continued to receive support from top party organs as well as through China’s government ministries and regulators (e.g., in the recommendations for the 15th Five-Year Plan 2026-2030). Specific progress was made in enhancing the standardisation of green finance through a new unified green taxonomy (previously, China had several green finance taxonomies, e.g., credit and bonds) and a statistical system. China also strengthened green insurance, impacting both the insured assets and the invested assets of insurance companies. Key developments included the expansion of the emission trading system to encompass steel and other sectors, along with a commitment to shift from intensity-based to absolute emission caps within the next five-year plan. Transition finance continues to play a vital role, though progress in standardisation has been gradual.

The application of green finance, measured by metrics such as green bonds issuance or green credit utilisation, remained generally stable over the past year, with growth in green credit, a recovery in green bonds from a low in 2024, and a stable outlook for green funds. As in previous years, it is worth noting that labelled green finance represents only a fraction of China’s overall financial system, with green bonds accounting for about 1% of all issued bonds and green loans comprising about 16% of all loans.

Building on the previous reports for 2021-22, 2022-23, 2023-24,and 2024-25 this brief analyses China’s green finance policies in 2025, identifies key trends, and recommends actions to further scale green finance for 2026. It serves as a snapshot of key developments and uses specific examples to illustrate China’s green finance trends and directions. It is not intended as a comprehensive guide to Chinese green finance and its developments.

Key developments in green finance policy

China’s overall policies supporting green transition and development strengthened in 2025. Both the Fourth Plenum (October 2025)[4] and the CPC Central Committee’s Proposal on the 15th Five-Year Plan (issued in October 2025) emphasise the carbon reduction goals and green industrial development, including the goal to “vigorously develop science and technology finance, green finance, inclusive finance, pension finance, and digital finance”.[5]

The following sections highlight and analyse green finance policy developments in China based on the five pillars for green finance development outlined by the PBoC since 2021:[6]

- Improve the green finance standard system including the new green finance taxonomy;

- Strengthen regulation and disclosure requirements;

- Enhance the incentive and restraint mechanisms;

- Enrich the product and market system; and

- Expand international cooperation and lead the setting of international standards for green finance.

Green taxonomy

2.1.1 Green taxonomy

The People’s Bank of China (PBoC), the China Banking and Insurance Regulatory Commission (CBIRC), and the China Securities Regulatory Commission (CSRC) jointly issued the Green Finance Support Project Catalogue (2025 Version), effective October 1, 2025. This represents a crucial step in transitioning China’s green finance standards system from multiple parallel tracks toward unification.

Hong Kong’s Monetary Authority (HKMA) launched a public consultation on the prototype for Phase 2A of the Hong Kong Sustainable Finance Taxonomy, with plans to eventually incorporate it into banking regulatory policies. The updated taxonomy adds manufacturing and information and communications technology sectors, expanding coverage from 4 to 6 industries and increasing economic activities from 12 to 25. It introduces definitions for “transition” and “climate adaptation” categories for the first time, specifying that transition activities should achieve significant emissions reductions in the short term

Statistical systems

n April 2025, the PBoC, National Financial Regulatory Administration (NFRA), CSRC, and the State Administration of Foreign Exchange (SAFE) jointly issued the Comprehensive Statistical System for the “Five Major Tasks” (Trial Version). This system establishes unified provisions for statistical subjects and scope, statistical indicators and definitions, statistical recognition standards, data collection, sharing, and release, as well as departmental responsibilities related to the “Five Major Tasks”.

Transition finance

Central and local governments and financial institutions are actively exploring transition finance standards for 2025:

- Jiangsu: In February, the Notice on Establishing a Transition Finance Support System to Facilitate Jiangsu’s Comprehensive Green and Low-Carbon Transition was issued. This document outlines the overall objectives for Jiangsu’s transition finance efforts. It proposes establishing a “1+N+N” transition finance support system, comprising 1 set of evaluation criteria for transition finance entities, N catalogues of transition finance-supported economic activities, and N types of transition finance products and service models, guided by the principle of “benchmarking internationally, grounded in reality, and demand-driven”.

- Guangzhou: The Guangzhou Transition Finance Implementation Guide group standard was formally released and implemented in December. This standard establishes a transition finance support project catalogue for three industries: chemical raw materials and chemical products manufacturing, pharmaceutical manufacturing, and rubber and plastic products manufacturing. A

- Hebei: Based on the revised Hebei Province Steel Industry Transition Finance Work Guidelines (2023-2024 Version), the Hebei Province Steel Industry Transition Finance Work Guidelines (2025 Version) were developed. This updated version further focuses on challenging issues within steel enterprises, establishing a comprehensive policy support system.

Disclosure standards

In September 2025, in accordance with the Corporate Sustainable Disclosure Guidelines—Basic Guidelines (Trial Version) issued in 2024, the Ministry of Finance (MoF), in collaboration with the Ministry of Foreign Affairs (MoFA), the National Development and Reform Commission (NDRC), the Ministry of Industry and Information Technology (MIIT), the Ministry of Ecology and Environment (MEE), the Ministry of Commerce (MOFCOM), the PBoC, SASAC, NFRA, and CSRC, formulated and issued the Application Guidelines for the Corporate Sustainability Disclosure Standards—Basic Standards (Trial Version). This guide consists of nine questions covering the value chain, reporting entity, information relevance, primary users of sustainability information, materiality assessment, the principle of proportionality, current and projected financial impacts of sustainability risks and opportunities, resilience of the enterprise’s strategy and business model to sustainability risks, and sustainability impact disclosure.

In October, China Central Depository & Clearing Co., Ltd. released six corporate standards, including the China Bond Green Finance Environmental Benefit Disclosure Indicator System, to complement the Green Finance Support Project Catalogue (2025 Version) issued by PBoC and other departments.

The General Office of CBIRC and the General Office of PBoC jointly issued the Implementation Plan for High-Quality Development of Green Finance in the Banking and Insurance Sectors. This document explicitly requires banking and insurance institutions to progressively establish and improve information disclosure mechanisms. The new standards aim to improve compatibility and consistency in environmental benefit disclosure for green financial products such as green bonds and green loans, further refining the green finance standards system.

Key developments in green finance instruments

Green loans

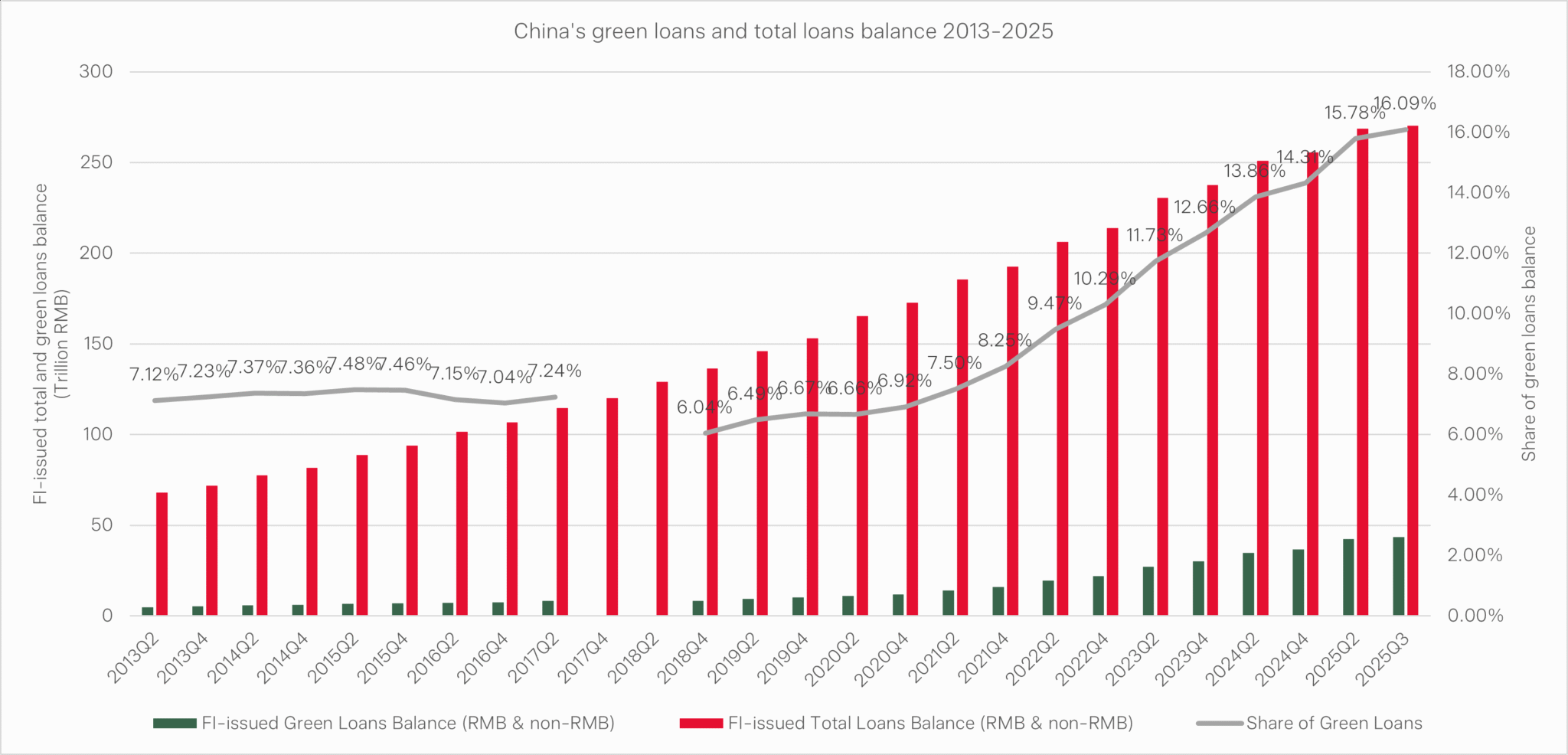

By the end of Q3 of 2025, the outstanding balance of RMB- and foreign-currency green loans reached RMB 43.51 trillion (USD 6.2 trillion), up 6.47 trillion (USD 0.9 trillion), or 17.5% from the beginning of the year. Green loan growth outpaced the growth of other loans. However, it should be noted that the 2025 figures are not directly comparable with earlier data on green loan balances, as the statistical coverage and eligibility criteria were revised at the beginning of 2025. Under the pre-2025 framework (see Table below), green-loan balances rose by 18.9% from the beginning of 2024 to end-Q3 2024, compared with 32.3% over the same period in 2023. The share of outstanding green loans in total lending increased to 16.09% by Q3 2025, from 15.78% in the beginning of 2025 (see Figure below).

| Green Industry Guidance Catalogue (2019 Edition) | Green Finance Supported Project Catalogue (2025 Edition) | |

| Positioning & applicability | Primarily an industrial catalogue that classifies “green” activities by industrial sectors and project types | Primarily a financial identification standard applicable across green financial products (e.g., green loans and green bonds). |

| Coverage | Six major sectors: energy-saving & environmental protection; clean production; clean energy; ecological environment; green upgrading of infrastructure; and green services. | Nine domains: energy saving & carbon reduction; environmental protection; resource recycling; low-carbon energy transition; ecological protection, restoration and utilisation; green upgrading of infrastructure; green services; green trade; and green consumption. |

| Identification logic | Functions largely as an activity list and is not designed specifically for financial statistics, so implementation often relies on interpretation and mapping. | Designed as a verifiable identification framework: item-level, tabular criteria with explicit industry codes, item names, eligibility conditions/standards, and notes, and includes fields such as “contribution to GHG emission reduction,” improving consistency and auditability. |

Green bonds

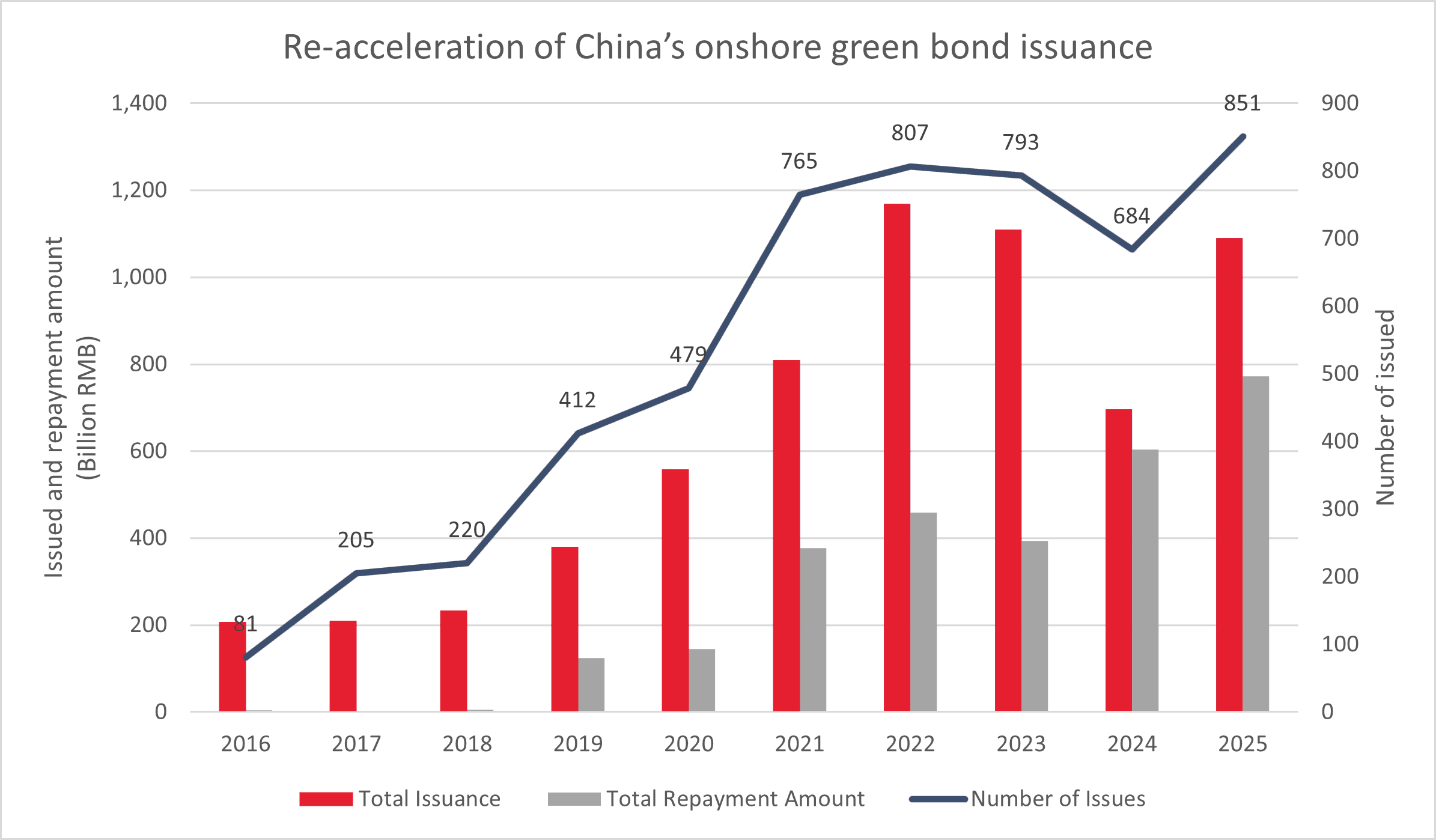

China’s onshore green bond market has seen multiple phases of growth and decline since 2016: Between 2018 and 2022, annual green bond issuance rose rapidly, but momentum weakened in 2023 and then fell markedly in 2024, with issuance volume down 31.62% year-on-year (YoY).

By the end of 2025, the slowdown reversed and issuance rebounded by 56.5% compared to the year ended 2024 to RMB 1.09 trillion (USD 154.72 billion). The annual number of green bond issues broadly followed the same trajectory, falling 13.75% YoY in 2024 before rebounding in 2025, rising 24.42% relative to the year ended 2024. Even so, yearly issuance has not yet returned to the historical peak reached in 2022.

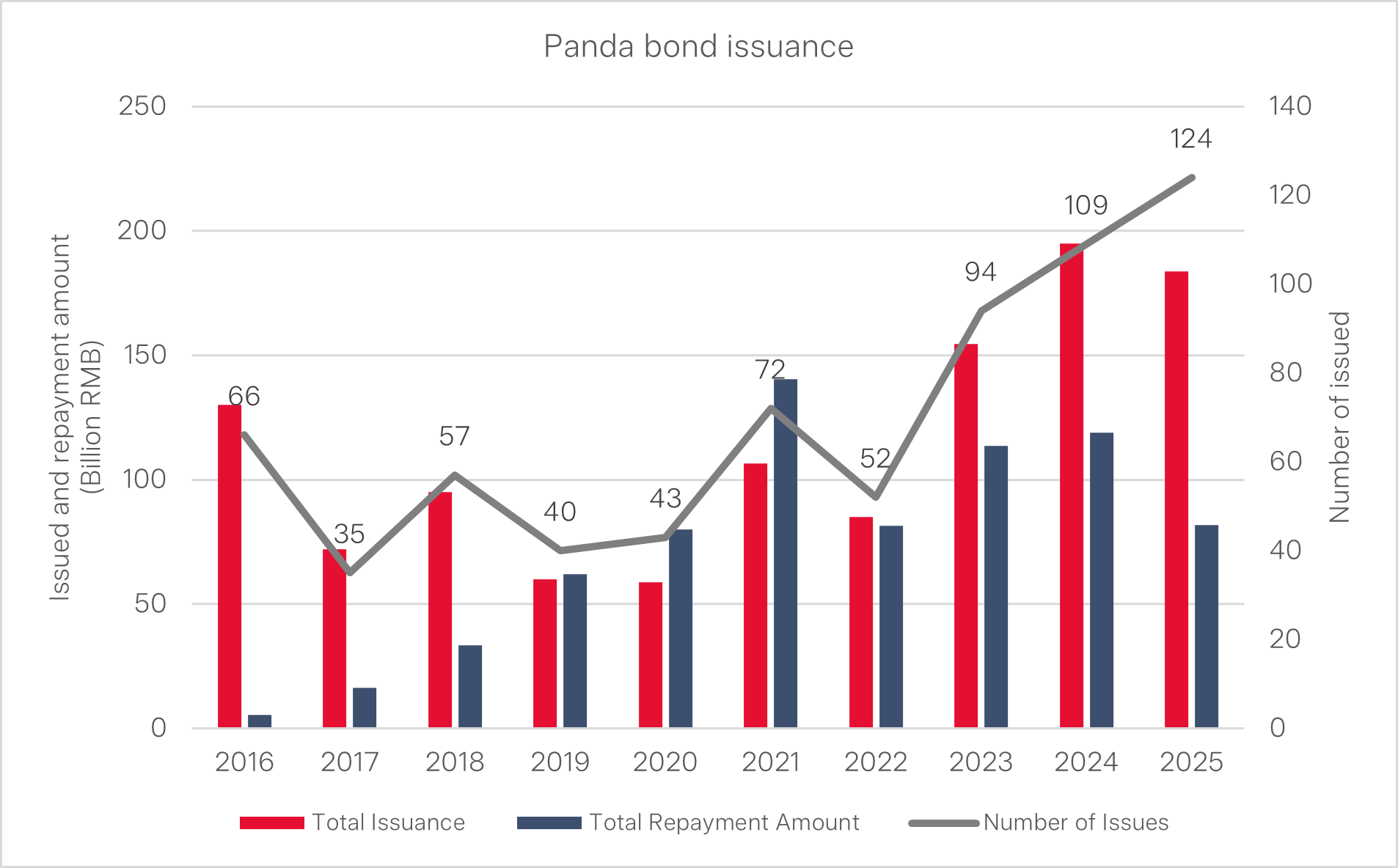

Panda bonds

Panda bonds (bonds issued by non-Chinese entities in RMB on China’s domestic bond market) remain attractive to international investors in 2025. By the end of December 2025, the issuance amount totalled RMB 183.56 billion (USD 26.04 billion), in line with the RMB 194.80 billion (USD 27.63 billion) issued in all of 2024 (see Figure below).

Against a backdrop of relatively lower interest rates within China with spillovers to onshore RMB bond issuances, Panda bond issuers were often able to secure funding at more favourable costs compared to other major markets.

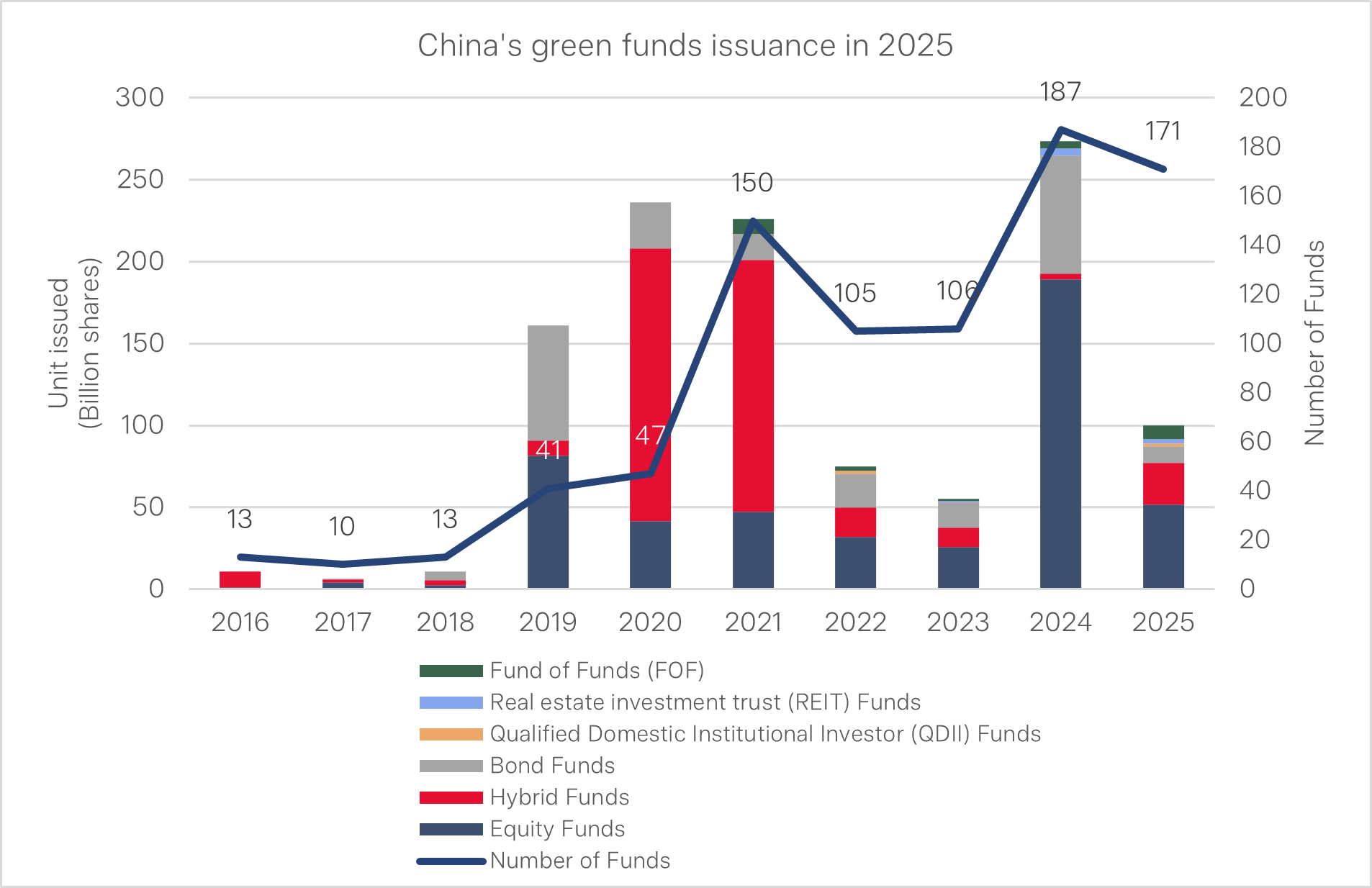

Green funds

After a rebound in 2024, new issuance activity in the green fund[65] segment slowed by the end of December 2025, primarily due to a contraction in new equity and bond fund launches (see Figure 11). Equity fund issuance fell from 189.26 billion shares in 2024 to 51.56 billion shares in 2025, a 72.76% decline, the sharpest drop among all fund categories. In contrast, hybrid funds increased by 22.07 billion shares in 2025, reaching 25.38 billion shares.

Green finance trends for 2026 and beyond

While 2025 can be viewed as a year of alignment and consolidation for China’s green finance framework, this section identifies seven trends that are likely to shape China’s green finance landscape in the future.

- Acceleration of transition finance as a key bridge between “pure green” and high-carbon asset phase-out based on catalogues

While the relevance of transition finance has grown since 2022 (including the 2025 release of transition finance standards for sectors such as steel, coal power, building materials and agriculture), this will be a core focus going forward. Drafting of standards for an additional seven sectors, including petrochemicals, chemicals, shipping and non-ferrous metals, is underway.

The challenge will be to balance risks of rapid transition on asset values and jobs, with the need to rapidly decarbonise to meet the “30-60” carbon goals and reduce de facto climate risks. A further challenge will be developing realistic transition standards that address current concerns while also spurring investment in future (uncertain) technology developments (such as green metals, green construction, green agriculture). Over the coming years, transition finance is therefore likely to grow into a core complement to “pure green” finance, especially for carbon-intensive industries.

2. Emphasis on climate-related disclosure, including data and control

In 2025, China issued Corporate Sustainability Disclosure Standard No. 1: Climate (Trial),taking a concrete step toward a domestic sustainability disclosure regime with climate at its centre. Larger listed companies and financial institutions are expected to pilot more structured climate-related disclosures aligned with international practice, while stock exchanges refine ESG and sustainability reporting guidelines for issuers. For labelled green and sustainability bonds, regulators are tightening expectations on use-of-proceeds, impact indicators and external review.

However, to meet disclosure requirements, capacity for data and internal controls will be strengthened. The use of big data to prepare and validate disclosure statements will be expanded with significant investment opportunities for data providers and verifiers. A big risk remains greenwashing, with AI playing both an exacerbating role (in creating misleading reports) and a controlling role (for oversight).

3. Banking and insurance shift from product-level green offerings to portfolio-level transition strategies

The Implementation Plan for High-Quality Development of Green Finance in the Banking and Insurance Sectors explicitly positions green finance as a core pillar of the banking and insurance business. It calls for a higher share of green activities in total assets, stronger climate and environmental risk management, and reinforced support for energy transition, industrial upgrading and pollution control. In practice, this implies a shift from isolated “green credit products” toward portfolio-level targets, differentiated treatment of high- and low-carbon assets, and tighter links between underwriting, investment and ESG performance. Green and transition finance are likely to be increasingly embedded in institutions’ capital planning, internal pricing and incentive systems, rather than treated as add-ons.

4. Biodiversity and blue finance move from concept to standardised, scalable product

Chinese regulators in 2025 initiated pilot biodiversity finance project catalogues across multiple provinces and municipalities, focusing on nature-based solutions, ecological restoration and ecosystem services. The intention is to bring biodiversity-related activities into a framework that can be linked to loans, bonds and insurance products. At the same time, coastal regions and sectoral regulators are exploring standards and pilots for blue finance, targeting marine ecosystem protection, coastal resilience and sustainable ocean-related industries. Biodiversity- and ocean-linked financing instruments are likely to shift from ad-hoc innovations to more templated, replicable products that can be scaled via mainstream financial institutions.

5. Digital and AI-enabled infrastructure underpins “precision” green and transition finance

The policies in 2025 create a stronger foundation for digitalising green finance data and workflows. Leading banks, insurers and pilot zones are already experimenting with big-data platforms, distributed ledgers and AI models to improve project screening, real-time emissions tracking and scenario analysis. These tools are being linked to carbon-accounting systems, collateral registries and ESG risk-management frameworks, with the aim of lowering transaction costs and improving risk-pricing accuracy.

6. China to set green finance standards in Global South – and North

With the withdrawal of major economies (such as the US) and the withdrawal of private institutions from setting green finance standards, China will be looked up to as a standard setter. As the self-styled “largest developing country”, China aims to be a role model for green finance cooperation in the Global South, but without Western leadership, China will increasingly be seen as the global leader and standard setter based on its vast experience with green finance standards and implementation.

This does not mean that international collaboration on green finance (e.g., through ISSB) will be determined by China, but that China’s institutions have a stronger say in the direction of standard-setting.

7. Green finance becomes a key lever in climate diplomacy and South–South cooperation

China is increasingly presenting its domestic green finance reforms as part of its contribution to global climate and biodiversity goals and as a basis for deeper South–South cooperation.Official narratives around green finance emphasise consistency with the Paris Agreement and the Kunming–Montreal Global Biodiversity Framework, while reiterating principles such as “common but differentiated responsibilities” and respect for national circumstances. Green and transition finance are being woven into bilateral and multilateral initiatives, including green development funds, co-financing with multilateral development banks and taxonomy cooperation. In the future, China is likely to further link its taxonomy, disclosure system and transition finance standards with its positions in global climate negotiations, using green finance both as a domestic policy tool and as an external signalling device.

Fang Yang is an Associate Professor at Xiamen University in China and a visiting professor at the Griffith Asia Institute of Griffith University in Australia. She holds a PhD in energy economics from Xiamen University. Fang’s research focuses on energy economics, climate change economics, and the Green Belt and Road Initiative (BRI), with years of experience in energy industry management and extensive practical experience in government departments, as well as project research expertise. She has published 3 academic monographs and over 20 papers, and presided over more than 10 scientific research projects, including those funded by the National Social Science Foundation and the National Natural Science Foundation of China. In addition to her academic research, she has served as a consulting expert for the Energy Research Institute of the National Development and Reform Commission, China International Engineering Consulting Corporation, State Development & Investment Corporation Smart City Research Institute, and Global Data Asset Council in China.

Jinze LI

Dr. Christoph NEDOPIL WANG is the Founding Director of the Green Finance & Development Center and a Visiting Professor at the Fanhai International School of Finance (FISF) at Fudan University in Shanghai, China. He is also a Professor at The University of Queensland and the lead for Asia Pacific Industry Transitions.

Christoph was a member of the Belt and Road Initiative Green Coalition (BRIGC) of the Chinese Ministry of Ecology and Environment. He has contributed to policies and provided research/consulting amongst others for the China Council for International Cooperation on Environment and Development (CCICED), the Ministry of Commerce, various private and multilateral finance institutions (e.g. ADB, IFC, as well as multilateral institutions (e.g. UNDP, UNESCAP) and international governments.

Christoph holds a master of engineering from the Technical University Berlin, a master of public administration from Harvard Kennedy School, as well as a PhD in Economics. He has extensive experience in finance, sustainability, innovation, and infrastructure, having established the Green Belt and Road Initiative Centre at the International Institute of Green Finance (IIGF) in Beijing, having worked for the International Finance Corporation (IFC) for almost 10 years and being a Director for the Sino-German Sustainable Transport Project with the German Cooperation Agency GIZ in Beijing.

He has authored books, articles and reports, including UNDP's SDG Finance Taxonomy, IFC's “Navigating through Crises” and “Corporate Governance - Handbook for Board Directors”, and multiple academic papers on capital flows, sustainability and international development.

")